Bitcoin is moving deeper into US household finance as homebuyers squeezed by high borrowing costs and limited supply look for new ways to fund a down payment without selling their digital assets.

On March 26, Better Home & Finance and Coinbase launched a structure that lets eligible borrowers pledge Bitcoin or USD Coin (USDC) stablecoin to secure a separate loan for a down payment while still taking out a standard conforming mortgage on the home.

The arrangement brings crypto into one of the most closely watched parts of the U.S. credit system at a time when affordability pressures are already reshaping who can buy a house and when.

The timing is central to the pitch as Realtor.com’s 2026 report put the US housing supply gap at 4.03 million homes.

This comes as the average 30-year mortgage rate recently climbed to 7%, while total mortgage applications fell 10.5%, and purchase applications dropped 5.4%. At the same time, first-time buyers accounted for just 21% of the market in the latest National Association of Realtors profile.

Against that backdrop, lenders and crypto firms are betting that a growing class of would-be buyers has wealth in digital assets but lacks the cash liquidity needed to clear one of the biggest barriers to homeownership.

A new route into the mortgage market

The Coinbase-backed product is aimed at borrowers who want to retain exposure to crypto markets instead of liquidating holdings to raise cash for a down payment.

For many, that decision is about more than market timing. Selling crypto can also trigger a tax bill and force investors to reduce positions they view as long-term holdings.

Considering this, the structure is built around two loans at closing. The first is a standard mortgage on the property. The second is a privately financed loan secured by pledged crypto and used to fund the cash down payment.

Better says the 15-year and 30-year fixed mortgage options will be available, subject to credit approval, and that the loans are designed in accordance with Fannie Mae guidelines so that the mortgage remains a conforming loan.

That distinction is important. The product does not replace the traditional mortgage with a crypto loan. Instead, it wraps a crypto-secured financing layer around the down payment while leaving the main mortgage in a conventional format.

For borrowers using Bitcoin, the initial collateral value must be at least 250% of the loan amount in fiat. For borrowers using USDC, the initial collateral value must be at least 125%.

In practical terms, a borrower could pledge $250,000 in Bitcoin to unlock a $100,000 cash-down-payment loan, or $125,000 in USDC for the same result.

The companies are promoting the arrangement as a way to preserve ownership of digital assets while gaining access to the housing market. Better says both loans can share the same interest rate and amortization term, creating a single combined monthly payment.

Housing strain creates an opening

The product's appeal is tied directly to a housing market that has become harder to enter, especially for younger buyers.

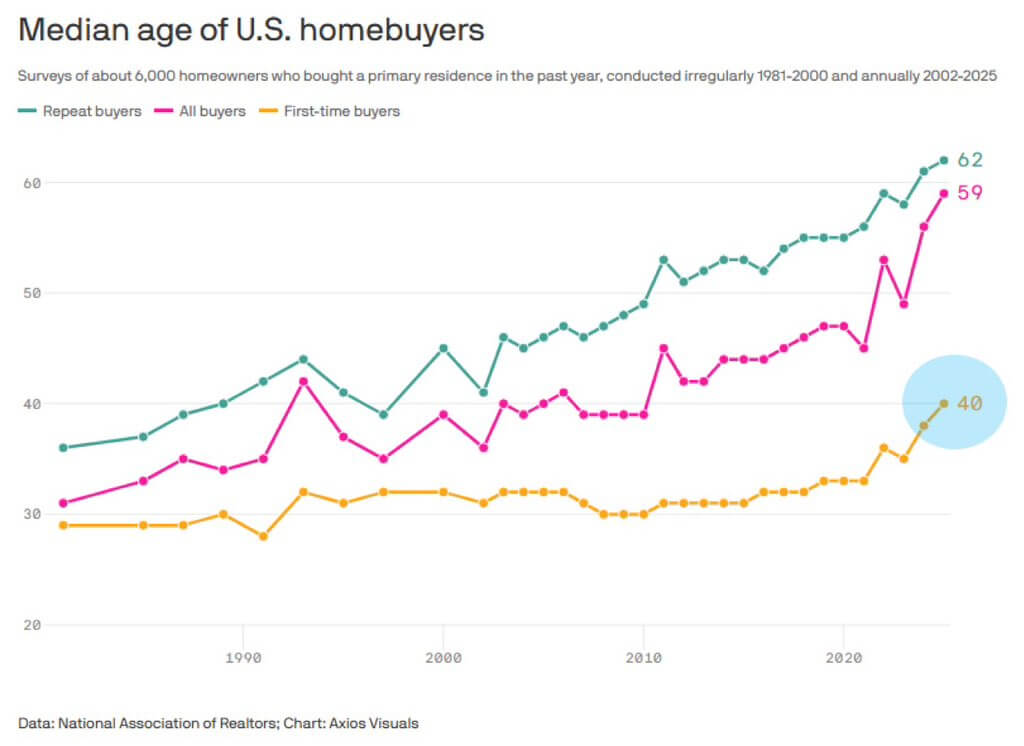

The median age of a first-time homebuyer reached 40 in 2025, according to the National Association of Realtors, reflecting the combined effect of high mortgage rates, elevated home prices, and limited inventory.

The pressure is even more severe for households lower on the income scale. The NAHB/Wells Fargo Cost of Housing Index for the second quarter of 2025 showed that a typical family needed 36% of its income for a mortgage payment on a median new home. For lower-income households, that share rose above 71%.

Those figures help explain why companies see an opportunity in linking digital assets to housing finance. Traditional underwriting relies heavily on documented income, credit history, and cash reserves.

That framework tends to favor households that have already built wealth through home equity, rising incomes, or long-established financial assets.

At the same time, millions of Americans have built positions in crypto. For context, around 20% of US adults, equivalent to 52 million people, hold some form of crypto asset, and the majority of them are young.

The NCA 2025 State of Crypto Holders report confirmed that 67% of token holders are 45 or younger, and 26% earn less than $75,000 a year.

That gives the product a clear target market: younger buyers with meaningful crypto exposure but limited willingness, or ability, to convert those holdings into cash at the point of purchase.

How the crypto pledge works

The companies have tried to structure the product to look less like a volatile crypto loan and more like a mortgage-compatible financing tool.

Borrowers who pledge Bitcoin or USDC are not subject to margin calls or top-up requirements if the market value of their collateral falls.

Better says market movements alone do not trigger liquidation. Instead, the pledged assets are only at risk if a borrower becomes 60 days delinquent on payments, a threshold the companies say mirrors the treatment of payment stress in conforming mortgages.

The crypto is held in custody for the life of the down payment loan and returned once that obligation is repaid. Borrowers cannot trade the pledged assets while they are locked up, which preserves ownership but restricts flexibility.

For USDC borrowers, the stablecoin can continue to earn rewards, which could help offset mortgage servicing costs and reduce the borrower’s net effective financing burden.

Meanwhile, the broader ambition goes beyond one mortgage product. Better and Coinbase say they intend, over time, to expand the range of eligible digital assets to include tokenized equities, fixed income, and other tokenized real estate assets.

This represents a sign that they see the mortgage offering as an early step in bringing on-chain wealth into mainstream consumer finance.

Policy support and political resistance

Meanwhile, this launch is arriving in a political climate that has become more receptive to crypto, but not without resistance.

Fannie Mae’s role, along with oversight from the Federal Housing Finance Agency, could help make such products more mainstream than earlier crypto-linked mortgage offerings.

Last year, FHFA Director Bill Pulte directed Fannie Mae and Freddie Mac to prepare to count crypto as an asset on mortgage applications, reflecting broader support for the digital-asset industry from the Trump administration.

That policy opening created room for commercial products built around crypto wealth, but it also drew criticism from lawmakers who view the idea as a new source of risk for housing finance.

Democratic senators, led by Elizabeth Warren, objected to the proposal, arguing that the current policy does not permit federally backed mortgage channels to consider cryptocurrency unless it has first been converted into US dollars and properly documented.

They warned that expanding underwriting criteria to include unconverted crypto could introduce fresh risks to both the housing market and the broader financial system.

That criticism goes to the heart of the debate around products like Better’s.

Supporters see them as a way to translate digital wealth into real-world access without forcing borrowers to sell assets and leave the market. Critics see a danger in bringing a volatile and still-developing asset class closer to the foundations of US home lending.

So, the final outcome may depend on whether crypto-backed mortgages remain a niche tool for affluent digital-asset holders or evolve into a broader financing channel for buyers shut out by the traditional down payment hurdle.

The post Homebuyers can now borrow against Bitcoin to get a mortgage without selling or liquidation risk appeared first on CryptoSlate.