Bitcoin price has again been knocked lower by an oil shock, higher Treasury yields, erased rate-cut expectations, and a massive Deribit expiry now due to land on top of that already-weakened market.

Roughly $14.1 billion in BTC options were set to expire today, Mar. 27, with another $2.2 billion in Ethereum contracts clearing the same morning, bringing the combined total to roughly $16.38 billion.

That is nearly 40% of Deribit's BTC open interest rolling off in a single session.

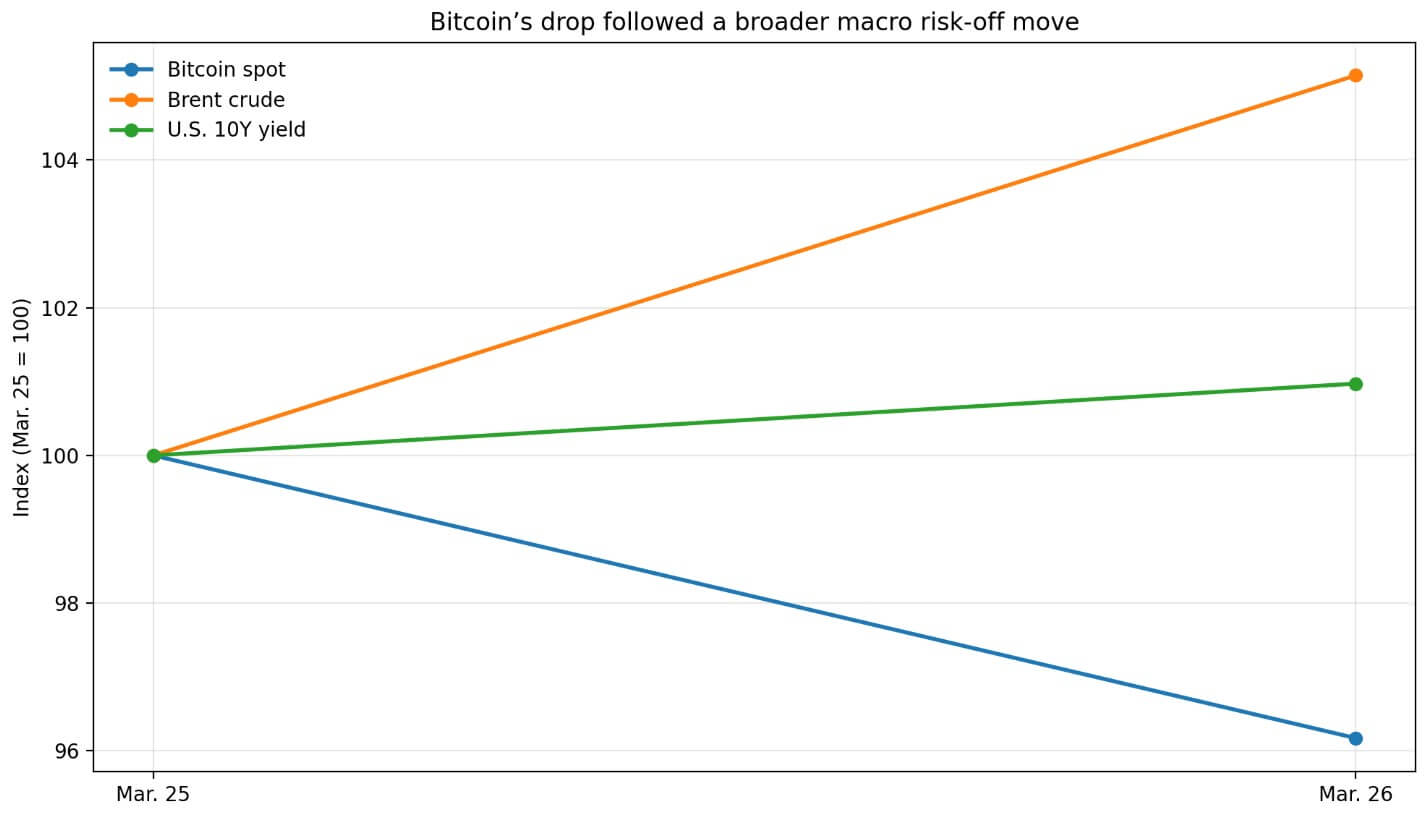

Reuters tied the broad risk-off to oil surging above $105, higher Treasury yields, a firming dollar, and markets pricing out Fed rate cuts for 2025 amid intensifying Middle East tensions.

Yesterday, BTC registered an intraday low of $68,127, while ETH reached $2,036. The expiry is arriving while the selloff is already underway as Bitcoin fell as low as $66,200 this morning, with Ethereum falling below $2,000.

Why the final 30 minutes carry the most weight

Deribit settles expiring contracts at 08:00 UTC using a 30-minute time-weighted average of its index, sampled every four seconds from 07:30 to 08:00 UTC.

That produces roughly 450 observations rather than a single closing print, making the delivery price harder to game but also meaning broad market moves during that window feed directly into settlement.

Simultaneously, the delta of expiring options and futures decays linearly toward zero across the same 30 minutes. Hedges are adjusting, rolls are compressing, and the pricing clock is running all at once.

That convergence draws disproportionate attention relative to the window's length.

A 2025 SSRN paper using Deribit data found BTC options activity clusters around 8:00-9:00 GMT, with the settlement-hour effect strongest on days with more expiring contracts and shorter maturities. Both cases apply here.

| Metric | Value | Why it matters |

|---|---|---|

| BTC options expiring | $14.16B | Core scale of Friday’s expiry |

| ETH options expiring | $2.22B | Adds to broader market impact |

| Combined BTC + ETH expiry | $16.38B | Shows total size of the reset |

| Share of Deribit BTC open interest rolling off | Nearly 40% | Highlights concentration in one session |

| Settlement time | 08:00 UTC, Mar. 27 | Fixed event readers can watch |

| Key pricing window | 07:30–08:00 UTC | This half hour determines the delivery price |

| Settlement method | 30-minute TWAP of Deribit index | Final price is based on an average, not one print |

| Sampling frequency | Every 4 seconds | Produces about 450 observations |

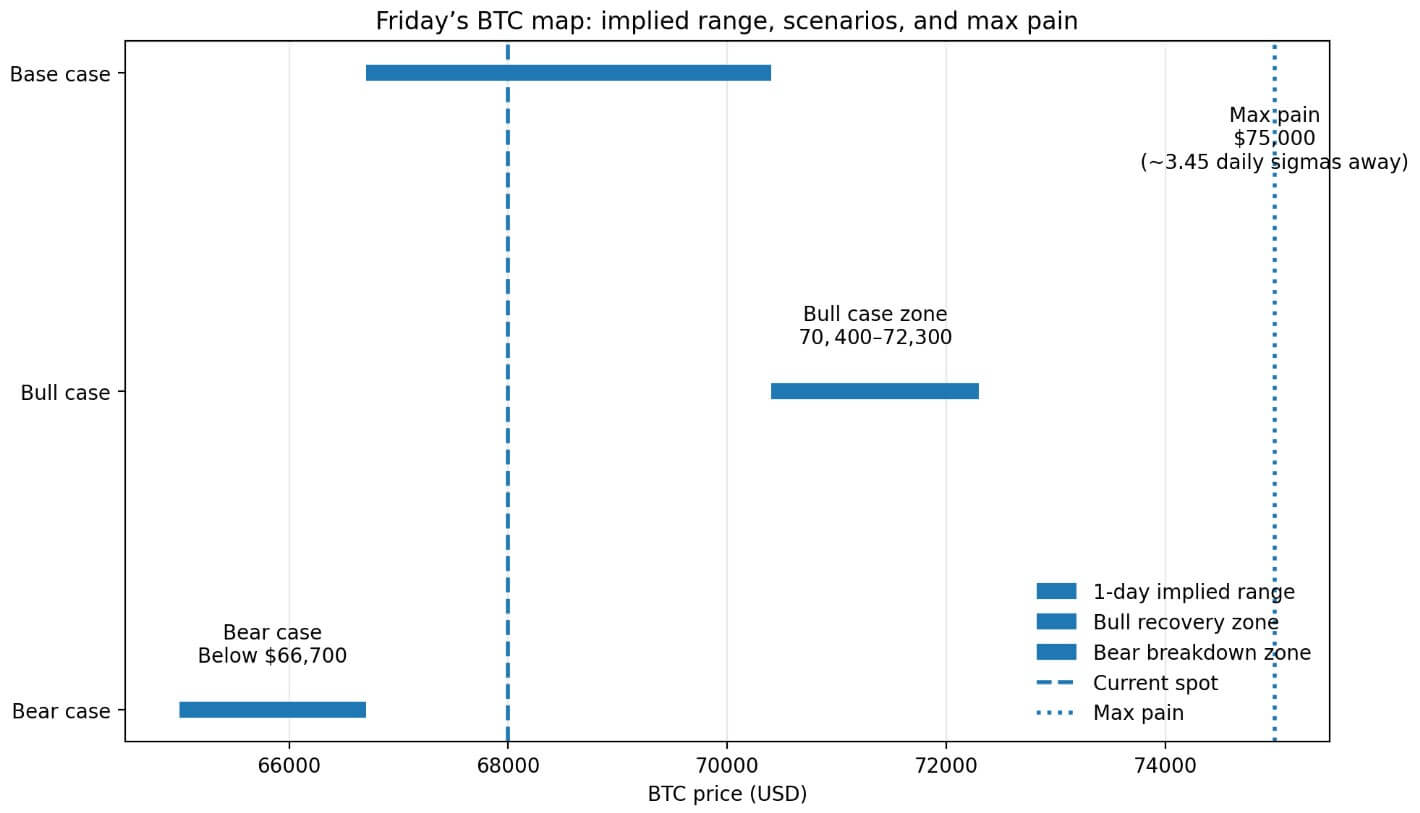

| BTC spot reference | Near $68,000 | Baseline for all comparisons |

| BTC max pain | $75,000 | Positioning reference, not a forecast |

| Put/call ratio | 0.63 | Indicates positioning skew |

| Distance from spot to max pain | ~9.4% | Shows max pain is well above current price |

| 7-day BTC ATM implied volatility | 52% | Basis for estimating near-term move |

| Implied one-day move | ~$1,866 | Frames realistic daily range |

| Implied 30-minute move | ~$269 | Frames realistic settlement-window move |

| Max pain distance in 1-day sigma terms | ~3.45σ | Suggests $75,000 is far from likely daily move |

| Max pain distance in settlement-window sigma terms | ~24σ | Shows max pain is extremely far from a realistic 30-minute move |

A 2023 paper found a clear Bitcoin expiration effect in volume, volatility, and returns around maturity, with the strongest effects shortly before or at expiry, though not uniformly across exchanges or contracts.

Reports citing Deribit data put Friday's BTC max pain at $75,000, with a put/call ratio of 0.63. From yesterday's spot near $68,000, that level was roughly 9.4% higher. Using the cited 52% seven-day BTC at-the-money implied volatility, the implied one-day move is approximately $1,866, placing $75,000 about 3.45 one-day sigmas above spot.

On a 30-minute implied-vol basis, the implied settlement window move is roughly $269, meaning $75,000 is nearly 24 settlement-window sigmas away.

At $75,000, max pain marks where open interest concentration is heaviest, roughly 9.4% above current spot and nearly 24 settlement-window sigmas away.

The macro arc that frames the expiry

BTC's recent resilience had already begun to fray before the recent drop.

Deribit-linked commentary on Mar. 25 described Bitcoin as relatively stable amid broader traditional market stress, marked by softer equities and tighter credit conditions.

By Mar. 26, that footing gave way: BTC slipped below $69,000 as oil shock, higher yields, and erased rate-cut hopes reasserted themselves.

Reuters reported global equity funds shed $20.3 billion in the week ended Mar. 18, while money market funds absorbed $32.57 billion, consistent with a broad defensive rotation.

Short-dated BTC implied volatility eased from 57% to 52% this week as temporary de-escalation headlines took hold, while put skew held. BTC 25-delta puts stayed roughly 5 volatility points richer than calls, and BTC futures-implied yields ran only 2%-3% across tenors.

The market has priced in a less immediate shock, while put skew and subdued futures yields keep the overall tone cautious. A $14.16 billion expiry now lands in that posture.

Because Deribit holds roughly 85% of the market share in BTC and ETH options, its settlement rules carry weight well beyond its user base. When one venue's 30-minute TWAP governs cash settlement for a notional that large, the mechanics of that window can ripple into the spot market.

The best and worst potential outcomes

A de-escalation headline on oil or geopolitics did not arrive before 07:30 UTC, stopping BTC from recovering toward the $70,400-$72,300 range, and expiry hedging damps downside rather than adding fresh selling.

The window could have acted as a stabilizer: with spot firming and fewer open puts in the money, dealer hedging flows turn less one-sided, and settlement TWAP prints above recent lows.

The expiry would have cleared without drama, and macro relief would have carried the price into the weekend. The tell would be spot recovering before the settlement opens.

However, oil and rates stress deepened into the morning. BTC broke below $66,700, the lower bound of the current one-day implied range, and now expiry mechanics add intraday noise to an already bearish market.

Dealer hedges on put positions require selling into a falling market, amplifying short-term moves around the settlement window. The 30-minute TWAP is printing a delivery price that reflects the full macro force, and now the expiry is accelerating the breakdown.

The macro environment that drove the move is now carrying into the post-settlement session.

Academic research and Deribit's own data confirm that the settlement hour drives flows and pricing mechanics.

What this morning's 07:30-08:00 UTC window focused on was hedging behavior, delta decay, and pricing methodology, compressed into a single, well-defined interval within a macro environment that has already knocked BTC lower by more than the implied daily range.

The post Bitcoin price just collapsed because the macro selloff collided with a $14 billion options expiry this morning appeared first on CryptoSlate.