Strategy (formerly known as MicroStrategy) is discovering that strengthening one part of its increasingly complex balance sheet can expose weaknesses elsewhere.

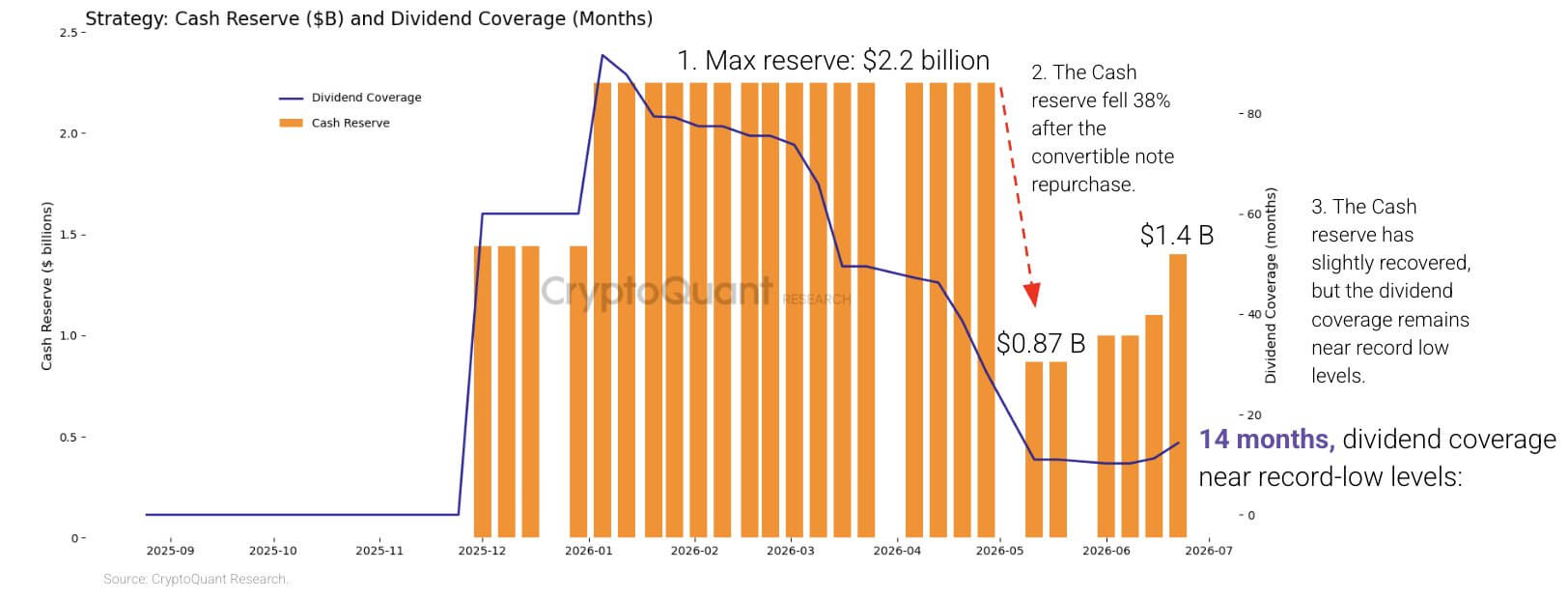

The Bitcoin treasury company spent $1.5 billion in May repurchasing convertible notes, reducing its debt but also draining cash that investors viewed as a backstop for its preferred-stock dividends. Weeks later, its Variable Rate Series A Perpetual Stretch Preferred Stock, known as STRC, fell to a record low of $82.50, or 17.5% below its $100 stated value.

Strategy has since started rebuilding the reserve by selling common shares. However, the response has sharpened a conflict at the center of Michael Saylor’s financing model: money retained to support STRC cannot simultaneously be spent buying Bitcoin, while raising that cash through MSTR sales dilutes existing common shareholders.

CryptoQuant said the pressure has become severe enough that the Saylor-led firm should suspend Bitcoin purchases until it restores its cash reserves and dividend coverage. Benchmark Equity Research, by contrast, views STRC’s decline as a market-driven repricing of the yield investors demand rather than evidence that the structure is failing.

The disagreement marks the clearest strain yet on Saylor’s effort to transform Strategy from a software company into an issuer of Bitcoin-backed “digital credit.”

Dividend costs outrun the cash reserve

STRC was launched in July 2025 as a perpetual preferred security designed to trade near $100. Strategy can adjust its dividend rate monthly to make the shares more attractive when they fall below that level.

The security has since become an important source of funding for Strategy’s Bitcoin purchases. That expansion, however, has created a rapidly growing recurring obligation.

CryptoQuant estimated that Strategy’s annualized preferred-dividend obligations have nearly quadrupled from about $300 million at the start of 2026 to $1.2 billion.

At the same time, the company’s cash reserves declined by 38% from the beginning of the year, with the sharpest reduction following the May repurchase of its 0% convertible notes due in 2029.

While retiring the notes removed a future claim from the balance sheet, it also reduced the pool of liquid funds available to cover dividends during a period when Bitcoin prices and Strategy’s securities were under pressure.

CryptoQuant said the company entered 2026 with enough cash to cover more than seven years of dividends. The firm estimated that coverage had fallen to about 14 months after Strategy rebuilt its cash position to $1.4 billion.

The analytics company estimated that Strategy would need about $2.8 billion to restore a 24-month reserve.

STRC allows Strategy to defer its dividends, but the payments are cumulative, meaning skipped distributions remain payable. A suspension could temporarily preserve cash while undermining investor confidence and making future preferred-stock issuance more expensive.

Strategy, therefore, has few painless options. Raising STRC’s dividend could support demand but would increase its cash burden. Retaining more capital would slow Bitcoin purchases, while additional MSTR sales would transfer more of the cost to common shareholders through dilution.

Meanwhile, Strategy’s Bitcoin treasury provides another potential source of liquidity, but using it now would also come at a cost.

CryptoQuant estimated that the holdings carried an unrealized loss of about $10.6 billion at prevailing prices. Selling during the downturn would crystallize some of those losses and challenge the company’s longstanding accumulation narrative.

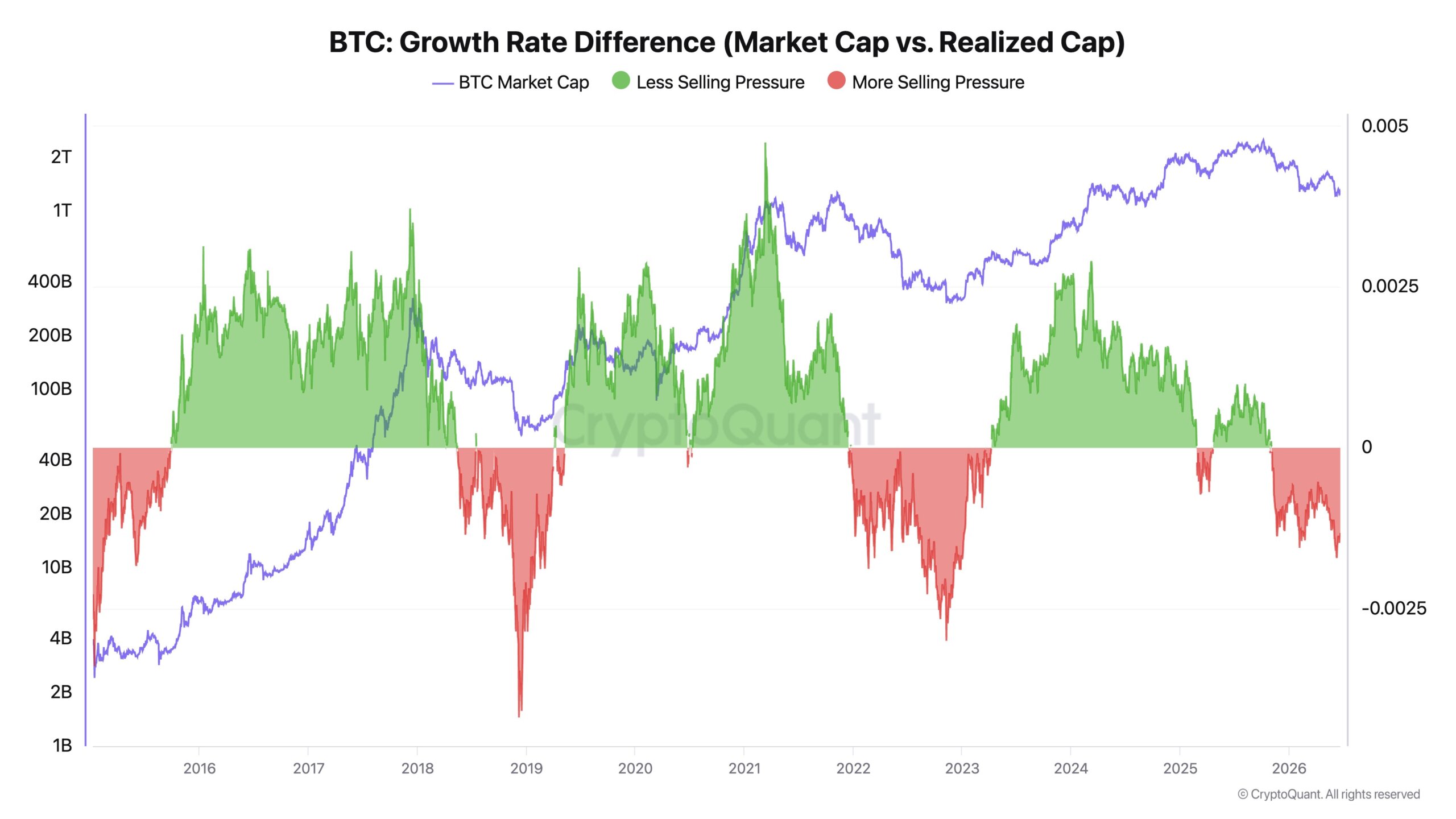

CryptoQuant Chief Executive Ki Young Ju said Strategy’s recent Bitcoin purchases appeared to be absorbing capital without producing a sustained increase in the cryptocurrency’s price.

He described the buying as more of a “liquidity sink” than a price catalyst and said the company should prioritize cash coverage before making further acquisitions.

Ju noted that Bitcoin’s realized capitalization had increased by $467 billion over the previous two years, even as its price declined by about 1%. He argued that the divergence showed fresh capital was largely allowing coins to change hands rather than driving a broad revaluation of the market.

Under conditions of limited selling, large institutional purchases can move prices sharply, Ju said. When selling pressure is elevated, the same demand may do little more than support an existing trading range.

He urged Strategy to replace its practice of buying whenever capital becomes available with a model-driven acquisition framework. He also called for rules that would allow the company to sell portions of its holdings during future market peaks, arguing that limited sales could reduce leverage, realize value for shareholders, and free up capital for purchases during later downturns.

Such an approach would represent a sharp departure from Saylor’s public commitment to persistent Bitcoin accumulation.

Common shareholders become the backstop

Meanwhile, Strategy’s latest fundraising showed which option management is currently prepared to use.

The company sold about 2.7 million MSTR shares last week, raising $335.5 million. It directed $300 million, or almost 90% of the proceeds, to its cash reserve and used the remaining $35 million to buy 520 Bitcoin at an average price of $67,068.

The allocation showed that rebuilding liquidity had temporarily taken priority over maximizing Bitcoin purchases. Strategy still expanded its holdings to 847,363 Bitcoin, purchased for about $64.01 billion at an average price of $75,651.

The cash injection also came with a larger share count. Strategy’s diluted shares increased to about 388.6 million from 386.1 million a week earlier. Its year-to-date BTC Yield, a company metric measuring changes in Bitcoin holdings relative to assumed diluted shares, fell to 11.8% from 13% four weeks earlier.

The decline does not mean Strategy owns less Bitcoin. It shows that Bitcoin holdings per assumed diluted share are increasing more slowly as the company issues additional equity.

That dynamic could become more pronounced if STRC remains substantially below $100. Issuing more preferred shares at unfavorable prices would become harder or require higher payouts, leaving common equity as Strategy’s most readily available source of capital.

MSTR shareholders would then be financing both the company’s Bitcoin purchases and the cash reserve supporting securities with senior claims on the balance sheet.

Supporters of Strategy’s model dispute the conclusion that its common-stock sales have weakened investors’ economic position.

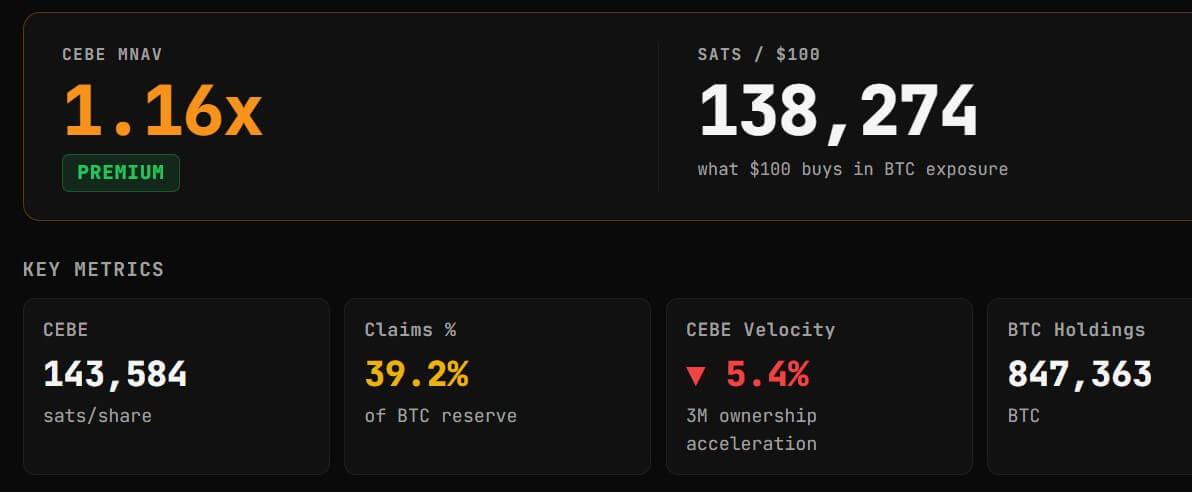

Adam Livingston, a pro-Strategy analyst, said the company added about 24,029 satoshis of Common Equity Bitcoin Exposure per basic share during the year despite issuing additional stock.

Common Equity Bitcoin Exposure, or CEBE, attempts to calculate the Bitcoin attributable to common shareholders after deducting debt, preferred stock, and other senior obligations. Livingston argued that Strategy used the proceeds from new shares to acquire enough Bitcoin to increase the net exposure supporting each basic share.

That does not mean the issuance was not dilutive. Existing shareholders still own a smaller percentage of the company after new stock is sold. Livingston’s argument is instead that the assets attributable to each share rose by enough to offset the increase in the share count.

Livingston’s conclusion also differs from the decline in Strategy’s reported BTC Yield because the two measures use different methodologies. Strategy’s metric relies on assumed diluted shares, while Livingston’s calculation uses basic shares and adjusts Bitcoin holdings for senior claims.

Data from CEBE Tracker placed Strategy’s CEBE multiple to net asset value at about 1.15 times, meaning MSTR continued to trade at a premium to the estimated net Bitcoin exposure attributable to common holders.

That premium remains central to Strategy’s model. As long as the company can issue stock above the value of the Bitcoin backing each common share and use the proceeds accretively, advocates argue that new issuance can increase rather than destroy per-share exposure.

The risk is that the premium narrows while cash requirements and preferred obligations continue to rise. Under those conditions, Strategy could still raise capital, but each transaction would generate less incremental value for existing common shareholders.

Meanwhile, this market pressure has impacted MSTR's price performance. Yahoo Finance data shows MSTR has fallen below the $100 mark, its lowest price level since March 2024.

Investors disagree over whether the model is breaking

CryptoQuant views STRC’s discount as evidence that Strategy’s liquid resources have failed to keep pace with its obligations. Benchmark analyst Mark Palmer sees the same decline as a conventional adjustment in the yield investors require.

Palmer rejected comparisons between STRC and failed stablecoins such as TerraUSD, noting that STRC is a perpetual preferred stock rather than an asset supported by an algorithmic peg. Strategy has said it intends to manage STRC near $100 but has not guaranteed that price.

At about $87, a dividend calculated at roughly 11.5% of the $100 stated value gives buyers a market yield of more than 13%. That suggests investors are demanding greater compensation for Strategy’s Bitcoin exposure, cash requirements and increasingly complex capital structure.

Benchmark maintained its buy rating on MSTR and a $570 price target, arguing that elevated STRC trading volumes showed active repricing rather than structural deterioration. The firm also pointed to Strategy’s Bitcoin treasury, worth roughly $55 billion at the prices used in its analysis, and the company’s continued ability to adjust dividends and raise capital.

Charles Edwards, founder of Capriole Investments, offered a more severe assessment. He said a business model dependent on continued Bitcoin appreciation to support dividends and yield products would eventually become unsustainable.

He noted:

“As long as his business model requires Bitcoin ‘number go up’ to survive and pay yield or dividends, it’s a ticking time bomb. Maybe not this cycle, but the music will stop.”

Edwards argued that Strategy should reduce its liabilities, unwind its yield products, and return to holding a less encumbered Bitcoin position. He also proposed acquiring digital-asset treasury companies trading at large discounts to their net asset values and eventually building operating businesses around Bitcoin lending, borrowing, and settlement.

Those proposals would involve significant obstacles. Repaying Strategy’s liabilities could require selling Bitcoin, issuing more equity, or both. A move into lending would also introduce regulatory, credit, and counterparty risks beyond those of a treasury company holding Bitcoin on its balance sheet.

Still, Edwards’ criticism captures the longer-term question facing the company: whether Strategy can continue expanding its capital structure without becoming increasingly dependent on higher Bitcoin prices and uninterrupted access to equity markets.

The competing assessments are not entirely incompatible. Strategy may hold sufficient assets to meet its obligations over the long term, even as it faces a near-term shortage of cheap, liquid capital.

Its latest fundraising decision reflects that distinction. Strategy could still access the common-stock market, but it had to direct most of the proceeds to rebuilding cash rather than accelerating Bitcoin purchases.

That trade-off is likely to define the next phase of Saylor’s experiment. Raising the STRC dividend would increase costs. Selling more MSTR would dilute shareholders. Selling Bitcoin could lock in losses. Suspending payments could undermine confidence in Strategy’s preferred-stock franchise.

For now, the company is choosing cash and dilution and asking common shareholders to absorb the cost of keeping its Bitcoin funding machine intact.

The post Saylor’s STRC Bitcoin machine is turning shareholders into its cash backstop – causing a dilution trade-off appeared first on CryptoSlate.