JPMorgan sees Wall Street’s shift toward private blockchains as a deeper threat to Bitcoin than Strategy selling its BTC.

JPMorgan warned that shifting tokenization, payments, and settlement onto closed networks could drain activity, liquidity, and capital from crypto while pushing valuations lower.

Hybrid public-private systems, tighter stablecoin rules, and Bitcoin’s staying power as digital gold could still upset that outlook.

Swift said 17 banks across six continents, including Citi, HSBC, Standard Chartered, UBS, Wells Fargo, and Itaú Unibanco, will begin testing live tokenized deposit payments on its new blockchain ledger, opening the door to round-the-clock transfers.

DTCC said on May 4 that over 50 firms, among them BlackRock, Goldman Sachs, Morgan Stanley, Nasdaq, and NYSE, joined its tokenization working group, with limited production trades planned for July 2026 and a full launch in October.

Where JPMorgan's case holds up

DTC already custodies over $114 trillion in assets, and DTCC subsidiaries processed $4.7 quadrillion in securities transactions in 2025.

If tokenized deposits settle within bank-controlled ledgers and tokenized securities reside within DTC's own infrastructure, that volume never touches the fee markets, liquidity pools, or token demand that Ethereum, Solana, stablecoin issuers, and RWA platforms depend on.

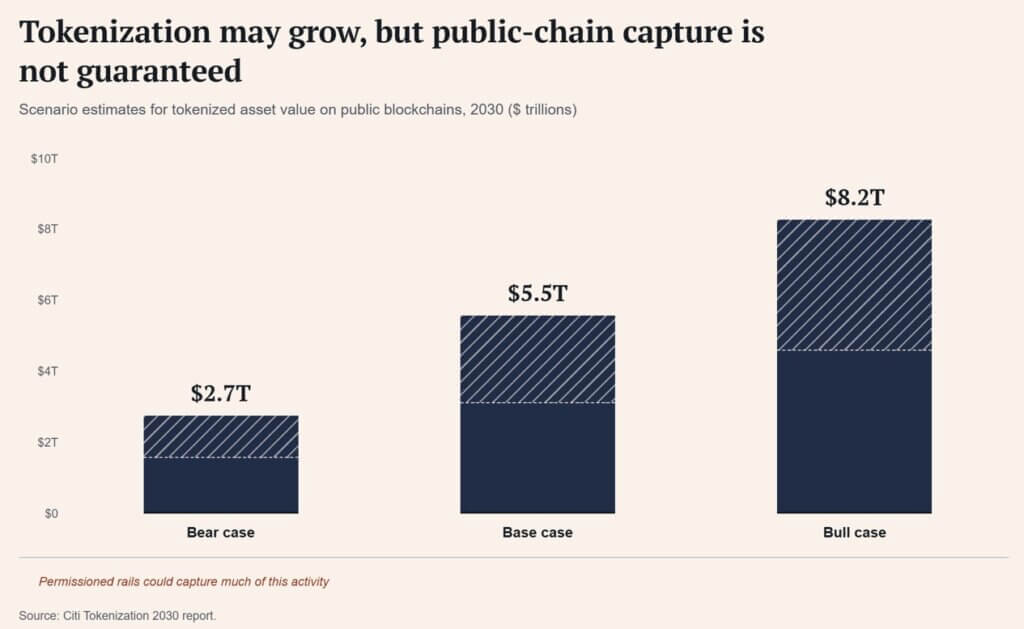

Citi's June 2026 Tokenization 2030 report puts the base-case tokenized asset market at $5.5 trillion by 2030, with a $2.7 trillion bear case and an $8.2 trillion bull case.

The BIS pointed out what that growth could look like in its June 2026 annual report: private permissioned networks can meet finance's regulatory and governance needs, and they also risk building walled gardens that dampen competition and innovation.

What Wall Street wants from Bitcoin

BlackRock's page for its spot Bitcoin ETF (IBIT) describes the product as exposure to Bitcoin's price through an exchange-traded structure that removes the custody and operational work of holding the asset directly.

IBIT held about $45.6 billion in net assets as of July 8, a figure that persisted despite a year-to-date NAV return of-28.93%.

Investors kept tens of billions parked in a fund that lost nearly 30% of its value this year, a pattern that reads like allocators holding scarcity exposure through whatever wrapper is easiest to custody.

Walled gardens are simple to understand once named: a bank-run ledger can freeze a balance, a permissioned chain can exclude a wallet, a tokenized deposit still answers to the bank that issued it, and a transfer-agent record can outrank the token sitting atop it.

Bitcoin offers a ledger that remains outside any single institution's control, existing alongside real limits, since Bitcoin is slow, expensive to move at scale, and built for something other than regulated securities settlement.

It makes Bitcoin the asset sitting outside the system that Swift, DTCC, and an expanding list of global banks are building.

| Feature | Private bank ledgers / tokenized deposits | Bitcoin |

|---|---|---|

| Core function | Faster institutional payments, settlement, and asset records | Scarce bearer asset outside bank control |

| Access model | Permissioned, KYC-gated, institution-mediated | Open network access |

| Control point | Banks, custodians, transfer agents, or market infrastructure providers | No single institutional operator |

| Reversibility / freezing | Balances or access can be frozen or restricted | Transfers are not controlled by one institution |

| Main advantage | Compliance, speed, liquidity efficiency, regulatory fit | Neutrality, scarcity, censorship resistance |

| Main weakness | Walled gardens, exclusion risk, limited openness | Volatility, scaling limits, custody/security risks |

| JPMorgan risk applies most to | Public-chain activity, fees, liquidity, and token value capture | Bitcoin only if investors treat it as generic crypto beta |

Bitcoin's third pitch

Bitcoin's pitch started as peer-to-peer electronic cash, then became digital gold once ETFs made it a line item in allocations.

The private chain era gives it a third framing: the scarce asset available to anyone once every other digital rail runs through a bank, a custodian, or a compliance gate.

The Federal Reserve held its target range at 3.50% to 3.75% at its June 2026 meeting, and the dollar index was near 100.93 on July 9 against a backdrop of geopolitical tension and inflation concern.

Stablecoins still carry the largest public chain payments footprint, with DeFiLlama showing about $311.9 billion in total stablecoin market cap against tokenized US Treasuries near $14.9 billion, a fraction of the roughly $30 trillion Treasury market itself.

The case above is a narrative argument, with real limits on what it guarantees for the price. JPMorgan's private bank noted that Bitcoin's volatility has been roughly four times that of global equities over the past decade and finds that a 5% Bitcoin allocation added 13% to portfolio risk, compared with 2% for an equivalent gold position.

Crypto firms are already preparing for the risks posed by quantum computing, with some estimates suggesting that a meaningful share of Bitcoin's supply could eventually be exposed if its cryptography is not upgraded.

In the bull path, tokenization grows toward Citi's higher range, and access stays gated, reversible, and bank-mediated at every step. Public chain tokens lose the settlement-layer premium that JPMorgan's argument targets, and Bitcoin's characteristics of being scarce, neutral, and issued by no institution shine through.

Private chain adoption starts to function as free advertising for the one ledger that stays independent of every bank building this system.

In the bear path, ETF outflows and a risk-off market dominate the narrative, and investors read private chain adoption as proof that banks now control the infrastructure crypto once promised to replace.

| Scenario | What has to happen | What it means for public-chain crypto | What it means for Bitcoin |

|---|---|---|---|

| Bull path: walled gardens make the exit more valuable | Tokenization scales toward Citi’s upper range, but access remains gated, reversible, and bank-mediated | Public-chain tokens lose part of the settlement-layer premium JPMorgan is targeting | Bitcoin’s contrast strengthens as scarce, neutral money outside bank-controlled ledgers |

| Bear path: banks win the infrastructure narrative | ETF outflows, risk-off markets, and weak liquidity dominate sentiment | Private-chain adoption is read as evidence that banks captured crypto’s original infrastructure promise | Bitcoin trades with crypto beta despite its distinct monetary thesis |

| Base path: both arguments coexist | Banks tokenize settlement while Bitcoin remains mainly an ETF-era allocation asset | Activity shifts to permissioned rails, limiting some public-chain upside | Bitcoin benefits narratively, but price still depends on flows, macro liquidity, and risk appetite |

Bitcoin trades down with the rest of the sector, regardless of how distinct its thesis is, with price tracking sector-wide risk appetite rather than the narrative underneath it.

For Bitcoin, the JPMorgan warning states the asset's oldest argument in real time: a financial system only a handful of institutions can program creates its own demand for the one asset none of them can.

The post JPMorgan’s $4.7T private blockchain warning just gave Bitcoin bulls fresh ammunition appeared first on CryptoSlate.