Money market Dolomite users are at risk of bad debt because the WLFI token is used as collateral under the WLFI Markets initiative.

By World Liberty's own description, WLFI Markets is only an interface, as Dolomite smart contracts handle the lending logic, collateral rules, and liquidations underneath.

The model explains how a Trump-linked venture could launch a branded lending market, with WLFI-supported collateral from day one, and why responsibility gets blurry the moment outside lenders start asking who approved the design and who bears the downside if it breaks.

The visible trigger is a large WLFI-backed stablecoin borrow, recently reported in the tens of millions, that pushed USD1 pool utilization past 100% and sent supplier rates sharply higher.

Dolomite's own documentation warns that risky collateral can expose the protocol to bad debt and describes “vaporizations,” the state in which liquidation exhausts collateral while debt persists and spreads across liquidity suppliers.

World Liberty built its lending product on top of Dolomite's protocol, as stated in its January 2025 launch materials, which included WLFI, ETH, cbBTC, USDC, and USDT as supported collateral assets and framed the product as a way to expand USD1 utility.

WLFI acquired a ready-made lending engine, enabled fast product launch, and provided immediate utility for its own tokens, while Dolomite owned the most failure-prone layer.

WLFI's overview notes that the interface does not custody assets, issue loans, or control protocol behavior. All supply, borrowing, repayment, withdrawal, and liquidation functions execute through Dolomite smart contracts.

Its terms state that users conduct transactions directly with WLFI Markets through Dolomite and are responsible for evaluating the risks of interacting with the brand.

That accountability hinges on brand on top and risk engine underneath, and was the product's architecture from the start.

| Function | WLFI / World Liberty side | Dolomite side |

|---|---|---|

| User-facing role | Branded product and interface presented as WLFI Markets | Underlying lending protocol and smart-contract infrastructure |

| Core contribution | Brand, distribution, token ecosystem, front-end access | Lending engine, market architecture, execution layer |

| What users interact with | WLFI Markets interface | Dolomite smart contracts underneath the interface |

| Lending mechanics | Says it does not itself custody assets or run lending logic | Handles supply, borrow, repay, withdraw, and liquidation functions |

| Collateral rules | Presents supported assets through the WLFI Markets product | Sets and enforces collateralization and risk parameters |

| Liquidations | Disclaims control over protocol behavior | Runs the liquidation engine and related protocol logic |

| Economics | Receives integration and marketing fees from Dolomite | Receives protocol activity, liquidity, and market usage |

| Liability posture | Says it is “only an interface” and users must assess third-party protocol risk | Can point to decentralized protocol design and user participation in the market |

| Why it matters | Captures branding and ecosystem upside | Carries the core risk-engine role underneath |

| Bottom-line takeaway | WLFI supplied the brand and token utility | Dolomite supplied the balance-sheet plumbing and risk management |

The front end and the back end

WLFI's disclaimer establishes its right to an integration and marketing fee from Dolomite. Reports noted that President Donald Trump's family held claims to 75% of net revenues from token sales and 60% of net revenues from operations.

By the time insiders took their cuts, calculations pointed to about 5% of the $550 million raised to date would remain with the venture to build the platform.

The collateral decision was a governed choice, documented in Dolomite's own governance materials. The money market's framework for asset listings requires price oracles, DEX liquidity, historical volatility, holder concentration, redemption mechanics during liquidation, and whether the protocol or DAO provides initial liquidity.

WLFI's concepts page says risk parameters are set by Dolomite governance and can change over time, while Dolomite's governance docs confirm that asset listings and parameter updates can be processed through DAO processes or by operators for management purposes.

The public materials establish that the WLFI configuration was acceptable, but leave the decision-makers unnamed.

The warning was public

Dolomite's risk documentation explicitly describes the guardrails it can apply to risky assets: supply caps, collateral-only modes, borrow-only modes, and strict-debt configurations.

The same docs warn that allowing risky assets as collateral can expose the protocol to bad debt if prices crash.

WLFI launched as supported collateral on the Ethereum mainnet on day one, leaving open the question of what governed the decision about WLFI's specific configuration if the guardrails existed.

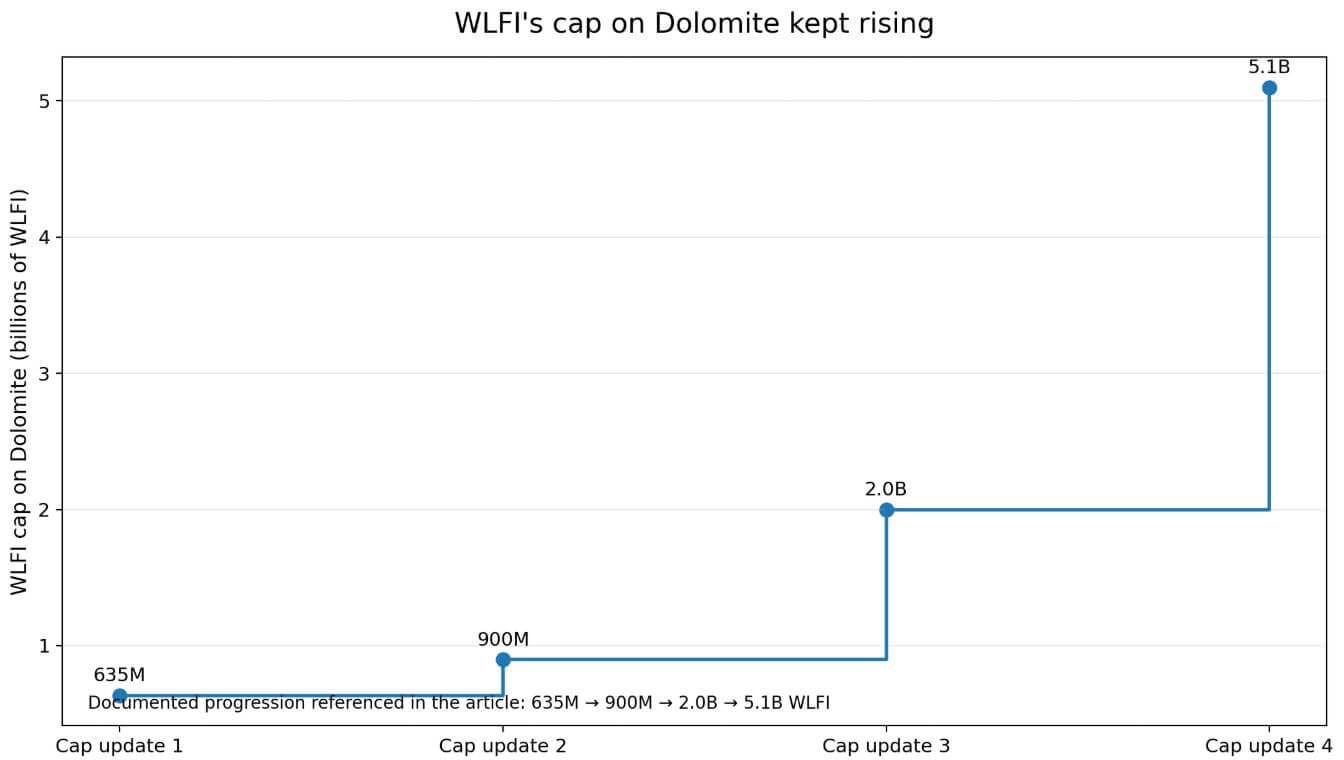

Dolomite's own admin-transaction repository shows that WLFI's market limits were repeatedly raised from 635 million to 900 million, then to 2 billion, then to 5.1 billion WLFI.

In the bull case, the structure survives and produces better architecture. Parameters tighten, the governance trail for who approved what becomes visible, supply caps or strict-debt modes limit WLFI-specific exposure, and the accountability split becomes an acknowledged feature.

Dolomite's own framework already encompasses all of those tools.

In the bear case, growth incentives keep outrunning guardrails. WLFI continues to benefit from token utility, brand distribution, and integration economics, and Dolomite absorbs the hard risk-engine role.

The next time utilization spikes, each side has a ready-made script: WLFI points to the interface-only language, Dolomite points to decentralized protocol design, and lenders absorb the gap between those disclaimers.

That outcome fits the current fee structure, the user-risk language in both sets of docs, and public records that stop short of naming the specific person who approved the WLFI collateral configuration.

The accountability gap

Ethics commentators flagged conflict risks around World Liberty as Trump oversees US crypto policy, Democratic lawmakers seek records tied to potential conflicts, and USD1 featured in a $2 billion Abu Dhabi-linked Binance investment.

The “Super Nodes” tier, which requires users to lock up the equivalent of $5 million in WLFI to access the protocol's team, added a dimension of preferential access. Those details raise the governance threshold for any venture operating at this level of political proximity.

A Federal Reserve staff note published on Apr. 8 reported that stablecoins had reached roughly $317 billion in aggregate market cap as of Apr. 6 and identified three specific vulnerabilities: more complex intermediation chains, greater vertical integration, and greater opacity about the source of stress.

The WLFI/Dolomite structure meets each criterion by providing a branded front end, third-party lending infrastructure, token incentives concentrated at the front end, and stablecoin pools beneath it.

| Party | What they gain | What they can disclaim |

|---|---|---|

| WLFI | brand expansion, token utility, integration/marketing fees | says it is only an interface |

| Dolomite | protocol usage, liquidity growth, lending volume | says users interact with a decentralized protocol |

| Outside lenders | high APR / incentive yield | little protection if liquidity vanishes or liquidation clears badly |

White-label crypto finance can scale distribution faster than it scales accountability, and the Fed's framework says that gap is exactly where stress amplifies.

Outside lenders supplied USD1 and USDC to shared pools, while WLFI supplied the brand, collected fees, and disclaimed liability for protocol performance per its own terms. Dolomite supplied the risk engine and, per its own docs, warned that risky collateral could create bad debt.

Accountability for whether WLFI met that standard was diffuse by design. If the position eventually produces a shortfall, each party has a documented basis to point elsewhere, while lenders absorb whatever gap is left by those disclaimers.

The post How Trump-linked WLFI set up a lending model where lenders will pay the price of failure appeared first on CryptoSlate.