Bitcoin's latest recovery has pushed the flagship digital asset back toward the $75,000 level, tracking a broader return in risk appetite as hopes for de-escalation in the Middle East lifted global equities to fresh records.

However, the move is running into a quieter constraint than geopolitics or crypto-specific sentiment: the bond market still shows a Federal Reserve that remains in no hurry to loosen policy.

That backdrop has become more important as the succession battle at the US central bank enters a more volatile phase.

The Senate Banking Committee has scheduled Kevin Warsh's confirmation hearing for April 21, while Jerome Powell's current term as chair ends on May 15.

Powell's term as a Fed governor runs until Jan. 31, 2028, and he said last month that if his successor is not confirmed by the time his chairmanship expires, he would serve as chair pro tem until that happens.

For crypto investors, that means the question is no longer only whether Warsh reaches the chair. It is whether the market begins to believe that a change at the top would actually alter the path of rates and liquidity.

The Fed's March meeting pointed in the opposite direction. Officials left the target range for the federal funds rate unchanged at 3.5% to 3.75%, said inflation remained somewhat elevated, and repeated that any further adjustments would depend on incoming data, the evolving outlook, and the balance of risks.

Bitcoin recovery meets a quiet ceiling

One of the most important macro variables for Bitcoin right now is the pricing of policy in the front end of the rates market.

CME said this week that March brought a dramatic repricing in short-term rate markets, with the 2-year Treasury yield swinging through a 50-basis-point range and FedWatch showing “no hike by December” as the base case for traders in 2026. That is not the profile of a market betting on a clean, aggressive easing cycle.

This metric is prescient because Bitcoin has spent most of this recovery trading like part of the broader global risk complex.

The same cease-fire hopes that pulled oil lower from recent peaks and helped send world equities back to record highs also revived expectations that inflation pressure from the Iran war might ease, a shift that helped gold and other non-yielding assets recover.

While Bitcoin has participated in that move, it has not escaped the larger debate over how restrictive US policy will remain.

The distinction is important. Crypto does not need a formal rate cut to respond. It needs the market to believe that financial conditions are becoming easier.

At the moment, that belief is still partial. Investors are willing to buy risk when oil falls, and war fears recede, but the rates market still reflects a Fed that wants more proof before it moves. That leaves BTC's rebound dependent on a macro repricing that has started only cautiously.

A succession fight with market consequences

Warsh's nomination was supposed to give markets a clearer line of sight on the post-Powell Fed. Instead, the handoff has become tangled in legal and political risk.

Treasury Secretary Scott Bessent said this week that he remains optimistic that Warsh will take the chair on time, but Republican Sen. Thom Tillis has vowed to block the nomination while a Justice Department investigation into Powell remains active. Sen. Elizabeth Warren has also urged the committee not to move forward under that cloud.

Powell has hardened that uncertainty rather than resolved it. In his March press conference, he said that if Warsh was not confirmed by the end of his term, he would remain chair pro tem, and that he had no intention of leaving the Board until the investigation was over “with transparency and finality.”

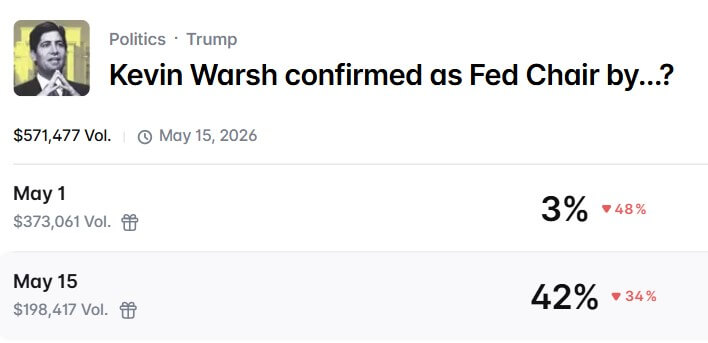

All of this uncertainty and stalemate have caused Warsh's May 15 confirmation odds on prediction markets like Polymarket to slip to 42%, down from highs of 80% earlier this year.

Meanwhile, President Donald Trump has since threatened to fire Powell if he stays after May 15, deepening the risk of an institutional clash just as markets are trying to price the next policy regime.

As a result, the practical consequence for markets is continuity. Even if Warsh is ultimately confirmed, any delay extends the life of the same cautious policy framework that has defined the Fed this year.

The current committee lineup remains Powell-led, and the March vote itself showed only one dissent, with Governor Stephen Miran preferring a quarter-point cut while the rest backed no change.

That shows at least one visible split, though the committee still looks broadly aligned.

Rates are only half the story

The case for restraint is clear in the data: the unemployment rate stood at 4.3% in March, according to the Labor Department, while core CPI was up 2.6% from a year earlier.

New York Fed President John Williams said on Thursday that the war in the Middle East is already feeding inflation pressures through higher energy and transport costs. St. Louis Fed President Alberto Musalem said a recent oil shock could keep core inflation near 3% for the rest of the year and leave rates on hold for some time.

But the Fed funds rate is only part of the transmission mechanism for crypto. The deeper issue is liquidity, which brings the balance sheet back into focus.

The Fed's total assets stood at about $6.69 trillion as of April 8, according to Federal Reserve data carried by FRED.

More importantly, the March policy directive showed the central bank is still increasing System Open Market Account holdings through purchases of Treasury bills and, if needed, other Treasuries with maturities of three years or less to maintain an ample level of reserves.

It is also rolling over principal payments from Treasury holdings and reinvesting agency principal into Treasury bills.

That plumbing is not the same as a full easing cycle, but it is important for markets built around liquidity narratives.

Warsh has been identified with a different mix: less tolerance for a large Fed balance sheet and more skepticism toward the bond-buying programs that expanded it.

In fact, Reuters has reported that he has criticized the Fed's balance-sheet management and pushed for less quantitative easing and a smaller portfolio. That combination can read as hawkish for liquidity in the near term, even if investors decide it is pro-growth over a longer horizon.

What crypto traders are watching now

The next clue comes quickly. Warsh's April 21 hearing will tell markets whether senators see him as a clean handoff candidate or as part of a broader fight over Fed independence.

Investors will be listening for his views on three linked questions: whether supply-driven inflation from the Iran war should be looked through, whether a lower policy rate can coexist with a smaller balance sheet, and whether he would preserve the Fed's cautious, data-dependent stance or try to redefine it.

After that, attention shifts back to the calendar that actually moves asset prices. The next FOMC meeting is scheduled for April 28-29, according to the minutes of the March meeting.

If Warsh is not yet confirmed, Powell remains the face of policy, and the market is likely to read any statement through the same wait-and-see framework it has been trading all year.

Even if Warsh does get through later, the bar for a durable crypto breakout will remain the same: traders must start to believe that front-end rates and reserve management are moving in a direction that loosens financial conditions rather than simply preventing stress.

That is why the quiet signal counts more than the loud one. Bitcoin can rise on truce headlines, ETF demand, and improved risk appetite, and all three have helped it recover.

However, unless the rates market begins to price a softer Fed path, or at least a more accommodative liquidity backdrop, the rally remains exposed to the same ceiling that has constrained it for much of the year.

For Bitcoin, the headline drama is in Washington. The more important variable is still trading on the short end of the US curve.

The post Bitcoin’s recovery hits a Fed ceiling with no sign of cheaper money appeared first on CryptoSlate.