Bitcoin’s recent price rebound faltered as the advance gave long-term holders and recent buyers an opportunity to sell before the cryptocurrency reached its next major resistance zone.

Data from CryptoSlate shows that the largest digital asset crossed $65,000 on Wednesday for the first time in about a month, then retreated under $63,000 as of press time. The move followed softer US inflation data and marked Bitcoin's strongest response to favorable economic news in weeks.

The retreat came even as several market indicators turned more constructive, setting up a test of whether recovering demand can absorb the supply emerging during rallies and carry Bitcoin above $70,000.

Long- and short-term holders constrain Bitcoin's recovery

Bitcoin’s failure to hold above $65,000 showed how quickly the rebound was drawing supply from investors on both sides of the recent downturn.

Bitcoin has traded below the realized price of the 18-month-to-two-year UTXO cohort since early June, according to CryptoQuant data. The measure estimates the average price at which coins in the group last moved and serves as a proxy for their break-even level.

That moving cost basis has since risen to about $80,800 as coins enter and leave the cohort, leaving many of its holders with substantial unrealized losses at current prices.

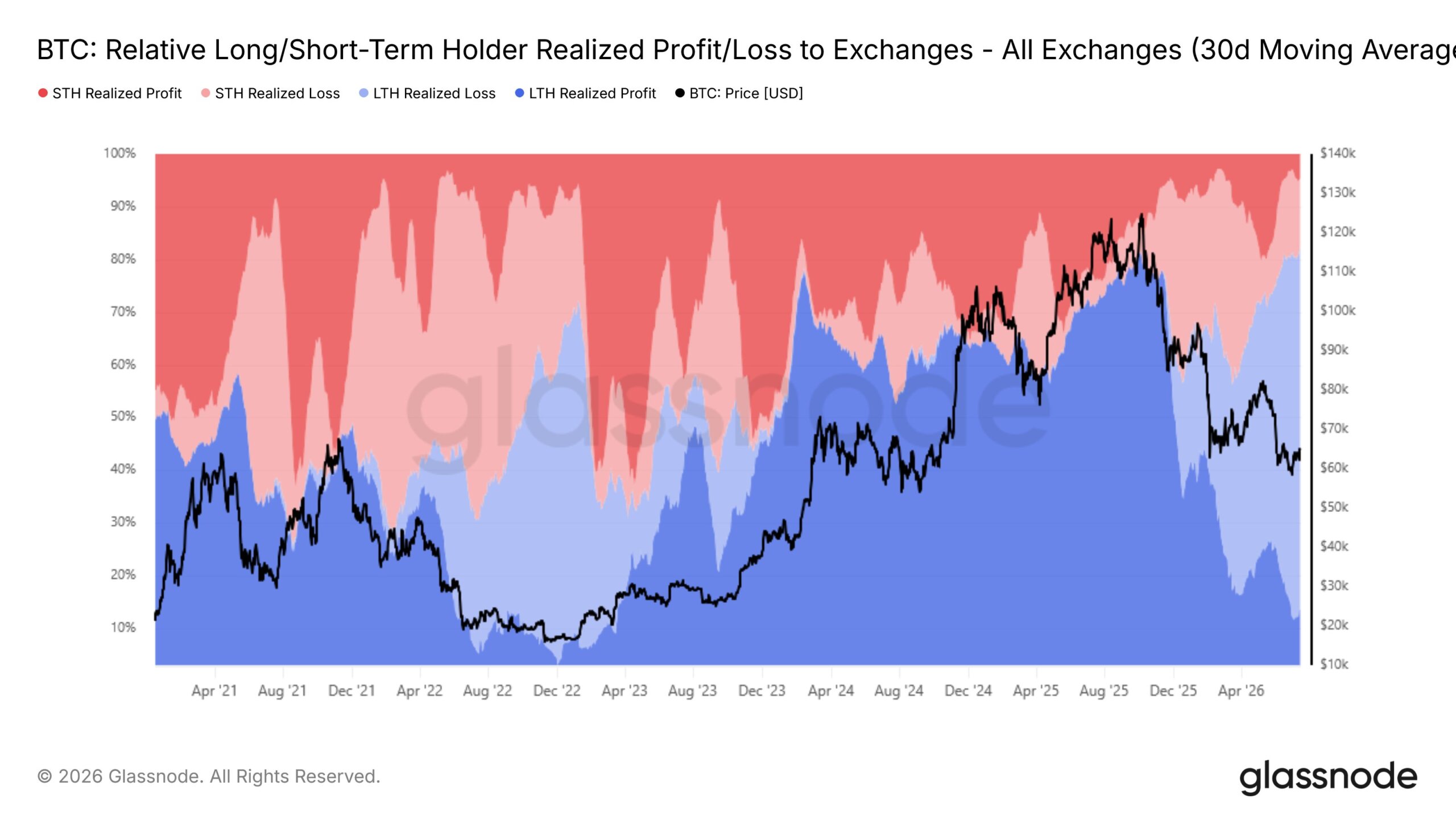

Long-term holder realized-loss volume increased as Bitcoin approached $66,000, Glassnode data showed. This rebound allowed underwater investors to sell at smaller losses than they faced when the cryptocurrency traded below $60,000.

Glassnode stated:

“Currently, more than 65% of exchange inflows are attributable to long-term holders realizing losses, a reading consistent with prior bear market phases where this cohort dominated the sell side.”

The data suggest that some holders used the rebound to reduce exposure rather than wait for Bitcoin to return to their estimated break-even price, adding supply to a market already struggling to extend its response to softer inflation data.

At the same time, short-term holders were selling into the same recovery for the opposite reason. Investors who accumulated Bitcoin near the June lows began taking profits at volumes last seen around the market's May peak.

The two groups entered at different prices and are recording different outcomes. Long-term holders are reducing losses, while recent buyers are protecting gains, but both are supplying Bitcoin as it attempts to move higher.

Their combined selling has added pressure while Bitcoin remains below the short-term holder cost basis near $69,000, where another group of recent buyers would return to break even. That level sits near a large concentration of options exposure between $70,000 and $80,000, creating overlapping sources of potential resistance.

ETF inflows return as Bitcoin's market regime improves

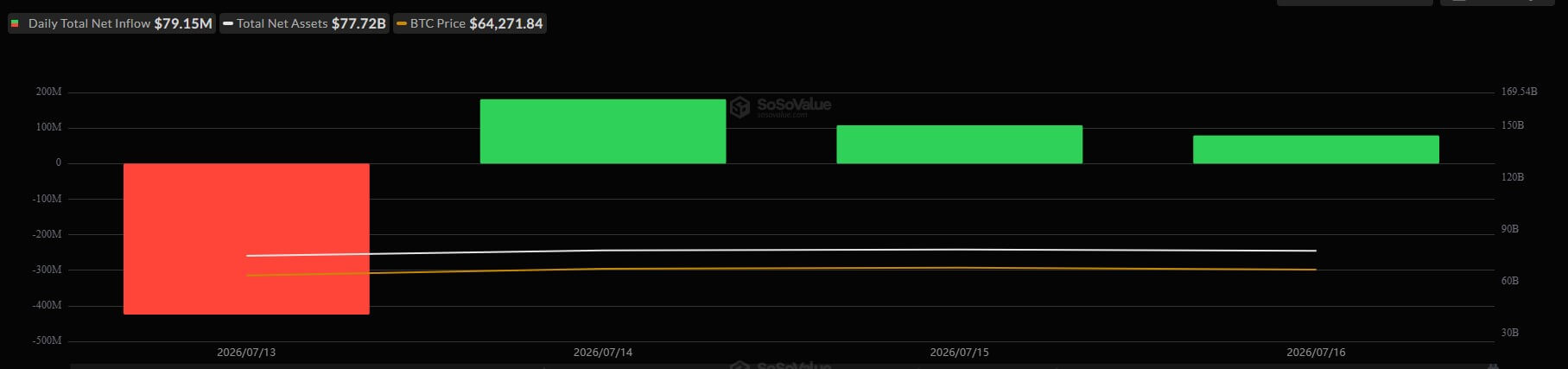

The selling pressure has not erased signs of improving demand, with US spot Bitcoin exchange-traded funds attracting money for three consecutive sessions after the week began with a sharp withdrawal.

The funds recorded $181.1 million of net inflows Tuesday, $107.7 million Wednesday and another $79 million Thursday. The combined $367.8 million recovered almost 87% of Monday’s $424 million outflow, leaving the week with a net withdrawal of about $56 million.

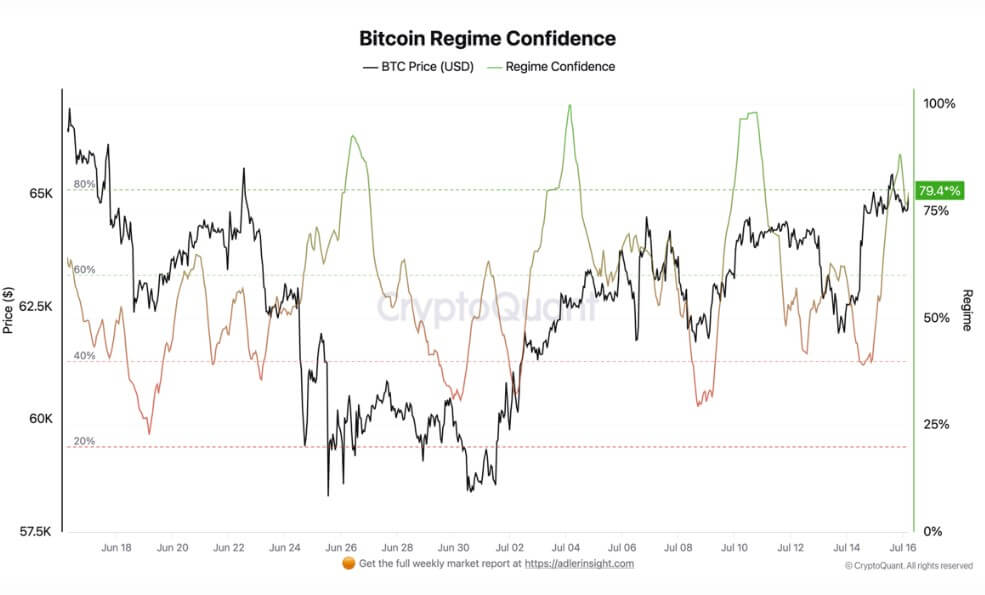

The improvement has coincided with a bullish turn in CryptoQuant analyst Axel Adler’s Bitcoin Regime Score, which combines taker flows, open interest pressure, funding rates, ETF activity, exchange flows and the price trend.

The indicator has risen to 34.7 on a scale from -100 to +100. It fell to -42.9 on June 26, when Bitcoin traded near $58,300, but has rarely remained below zero since July 2.

The score spent roughly four-fifths of the past week in positive territory, compared with about three-fifths of the full month. It reached 65.3 on July 10 before retreating toward neutral four days later, but the pullback did not develop into a sustained negative reading.

Agreement among the model's components has also strengthened. Regime Confidence rose from 54.9% to 79.4% over the past 24 hours, placing it just below the model's 80% high-confidence threshold.

Its seven-day average has increased to 64.3%, compared with 57.3% for the full month. The rise in both the score and confidence suggests that the improvement is supported by several market inputs rather than by a single unusually strong component.

The indicators have yet to produce a decisive price breakout, however. A return in the Regime Score above 50, accompanied by confidence near 80%, would provide stronger confirmation that the recovery had regained momentum.

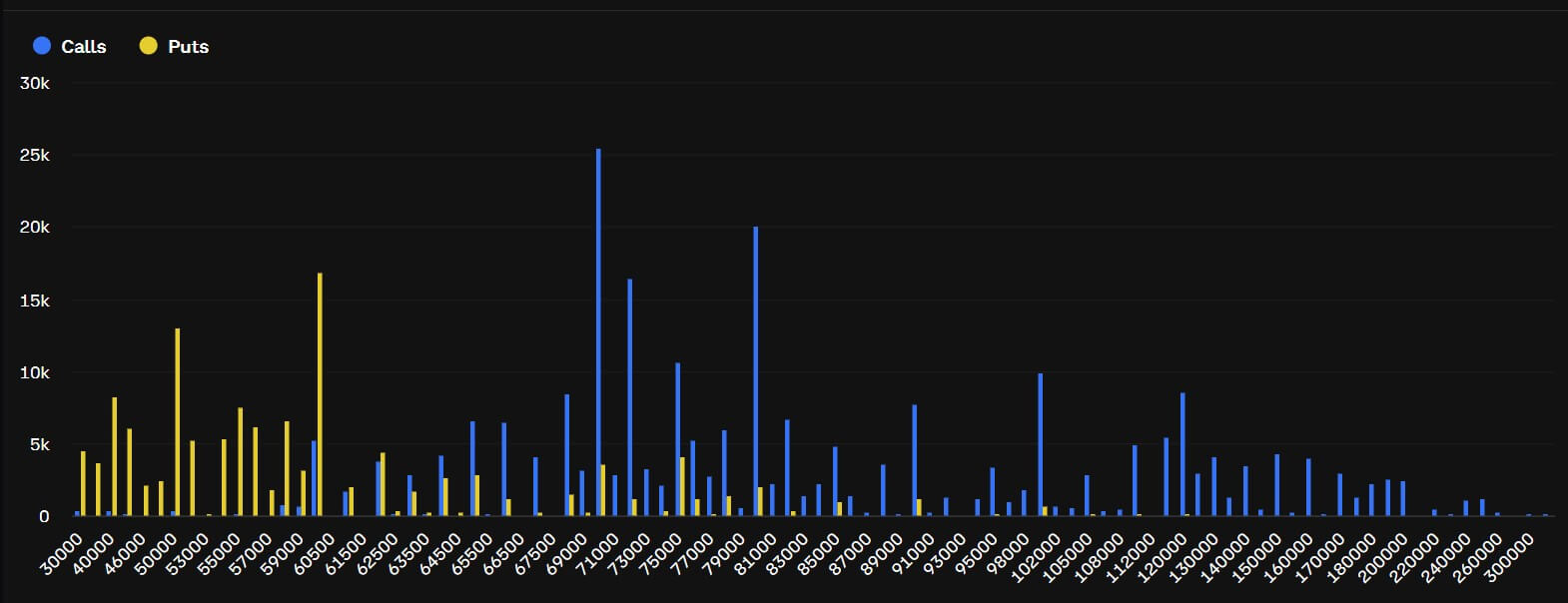

Options exposure stacks up above $70,000

The improving regime now faces its first major test in a region where short-term holder supply overlaps with a heavy concentration of call open interest.

Deribit data show about $1.6 billion of Bitcoin call open interest at the $70,000 strike, $1 billion at $72,000 and $686 million at $75,000. A further $1.2 billion is concentrated at $80,000.

Those four strikes account for nearly $4.5 billion in open interest, creating a broad options corridor above the current market price.

The short-term holder cost basis near $69,000 lies near that corridor. Bitcoin could therefore encounter selling from recent buyers returning to break even at the same time that options traders and market makers begin adjusting positions around the largest call strikes.

Open interest alone does not reveal whether the positioning reflects outright bullish trades, covered call sales, volatility strategies, or portfolio hedges. Every options contract also has both a buyer and a seller, making the totals an incomplete measure of directional conviction.

The concentrations nevertheless identify levels where hedging activity could increase as Bitcoin approaches the strikes, particularly around large expirations. Those adjustments can amplify price movements in either direction.

Bitcoin needs stronger demand to clear $70,000

Clearing the options corridor will depend on whether the recent improvement in demand translates into a broader, more sustained recovery.

US spot Bitcoin ETFs have recorded three consecutive sessions of inflows, but the reversal remains limited compared with the withdrawals recorded across the two largest funds over the past month.

Combined flows for BlackRock's IBIT and Fidelity's FBTC have averaged more than 1,250 BTC of net outflows per day over the past 30 days, Glassnode data showed. Trading activity across the ETF market has also declined, suggesting that participation remains subdued despite the recent inflow streak.

Bitcoin would therefore need continued spot and ETF buying to absorb sales from recent buyers returning to break even and older holders using rallies to reduce losses.

There are early signs that pressure from long-term holders may be easing. The cohort's 30-day average realized-loss volume has begun to retreat from its recent high.

Previous bear markets established firmer footing after that measure peaked and entered a sustained decline. However, the current rollover remains too brief to confirm that the heaviest distribution has ended.

Until demand strengthens and selling by holders eases more decisively, Bitcoin remains caught between improving market signals and supply that emerges during recoveries.

Failure to clear the overlapping resistance between $70,000 and $80,000 would return attention to the downside. Open interest in puts totals about $1 billion at $60,000 and $840 million at $50,000, creating another large options concentration below the current market.

The $60,000 level would become the first major test after another rejection, combining a large put concentration with an area where buyers previously defended the market.

The post Bitcoin buyers and bagholders are both selling into the rebound below $70,000 appeared first on CryptoSlate.