This month, Israel and Pakistan supplied a quieter test for crypto than the one playing out in US capital markets. What if the more important 2026 shift is happening where digital assets meet local money and bank accounts?

Israeli crypto firm Bits of Gold said Israel's Capital Market Authority approved the issuance and distribution of BILS, a shekel-pegged stablecoin, after a two-year pilot. Days earlier, the State Bank of Pakistan issued BPRD Circular Letter No. 10 of 2026, replacing its 2018 virtual-currency prohibition.

The Pakistan circular allows regulated entities to open bank accounts for PVARA NOC or licensed VASPs and their customers under defined compliance conditions.

Those two moves sit far from the US spot ETF cycle. Yet they point to the operational layer that decides whether crypto becomes more than an investment wrapper. The US has supplied legitimacy, liquidity, and a powerful digital-dollar debate.

Other jurisdictions are testing a different operating layer: whether crypto can connect to local money, bank accounts, merchant checkout, and enforceable market rules.

That distinction changes how global adoption should be evaluated. A Bitcoin ETF lets investors buy exposure. A regulated shekel stablecoin lets users hold a domestic currency on-chain.

A central bank circular that lets licensed crypto firms open accounts gives the sector a bridge back into supervised banking. The first validates an asset class. The second and third test whether crypto can become usable financial infrastructure.

The test remains early. BILS still needs proof of issuance and usage. Pakistan still needs licensed VASPs with actual bank relationships. Hong Kong's new licensees still need business launches.

The UAE still needs clearer public mapping between dirham-token announcements and Central Bank register entries. Still, the pattern is becoming harder to dismiss: in 2026, the practical crypto work is increasingly about where digital assets touch money, banks, merchants, and settlement systems.

Local money and bank access

Bits of Gold says the approved BILS project is a shekel-pegged stablecoin designed initially on Solana, with Fireblocks, QEDIT, EY, and the Solana Foundation involved in the pilot.

The policy signal is the local-currency component. BILS brings the shekel into an on-chain market still dominated by dollar stablecoins and asks whether a national currency can gain a programmable version without ceding the entire payments layer to USD tokens.

That is the monetary-sovereignty angle. Dollar stablecoins have become the working unit of much of crypto's settlement activity.

A shekel token, if issuance and adoption follow approval, gives Israel a way to test domestic-currency rails inside that same infrastructure. The result would be measured less by market attention and more by whether wallets, exchanges, payment firms, and regulated counterparties find a reason to use it.

Pakistan supplies the banking half of the opening. The State Bank of Pakistan circular is concrete because it replaces FE Circular No. 3 of 2018 and permits SBP-regulated entities to open accounts for PVARA NOC or licensed VASPs and their customers.

The circular also ties access to bank controls, documentation, monitoring, customer-risk checks, and compliance with Pakistan's virtual-asset framework.

That changes the operating surface for licensed crypto firms. Bank accounts are basic financial plumbing. They determine whether a regulated VASP can hold client money, reconcile flows, satisfy due diligence, and bring activity into monitored channels.

For a market such as Pakistan, which Chainalysis ranks among leading crypto adoption countries, banking access can decide whether usage remains informal or moves into traceable institutional structures.

Hong Kong offers a licensing comparator for the same rails-first pattern. On April 10, the Hong Kong Monetary Authority granted stablecoin issuer licenses to Anchorpoint Financial Limited and The Hongkong and Shanghai Banking Corporation Limited.

The HKMA register lists both with effective dates of April 10, 2026. That moves the jurisdiction from policy design to named licensed issuers, while leaving the business-launch and user-adoption tests ahead.

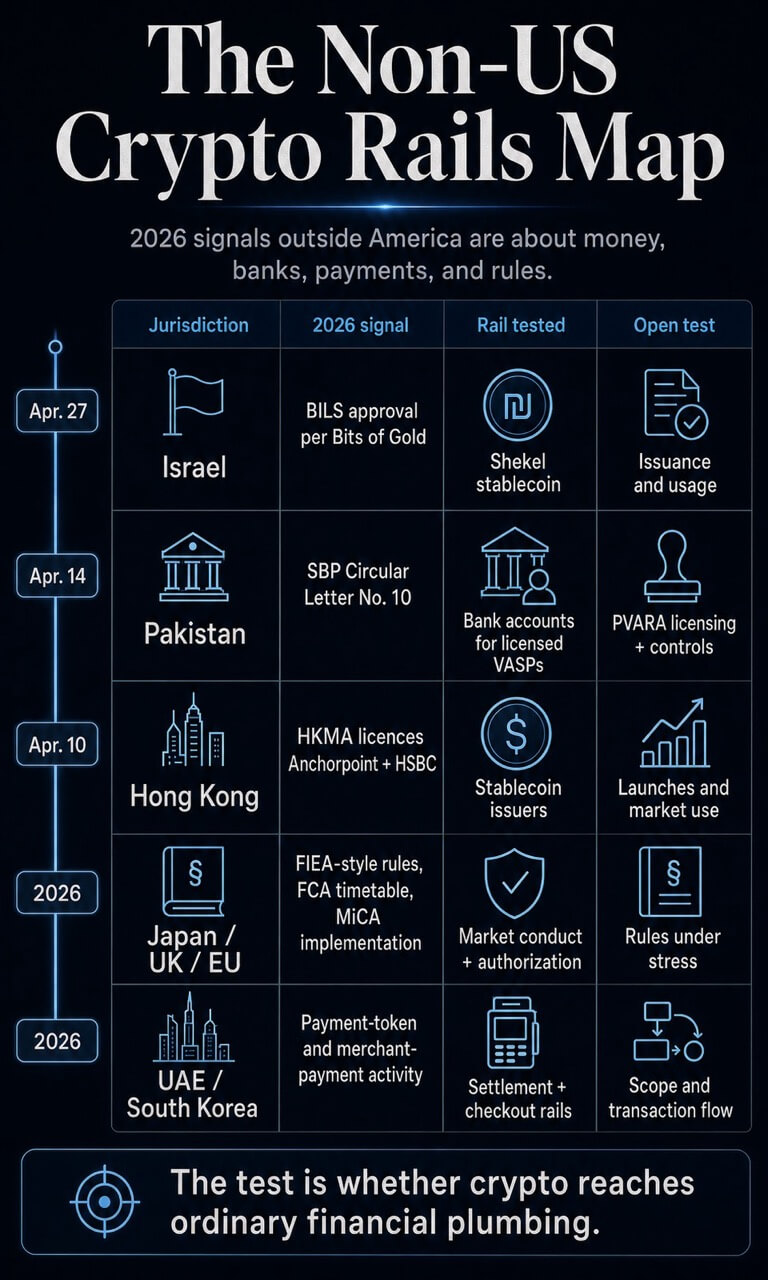

The early map is straightforward:

| Jurisdiction | 2026 signal | Rail being tested | Open test |

|---|---|---|---|

| Israel | Bits of Gold approval statement | Local-currency stablecoin | Issuance, redemption, and user uptake |

| Pakistan | SBP Circular Letter No. 10 | Bank accounts for licensed VASPs | PVARA licensing and bank controls |

| Hong Kong | HKMA stablecoin issuer licenses | Named licensed issuers | Launches and market use |

| Japan, UK, EU | Rulemaking and implementation clocks | Market conduct and authorization | How rules behave under stress |

| UAE, South Korea | Payment-token and merchant-payment activity | Settlement and checkout rails | Scope, transaction flow, and adoption |

Rulebooks are becoming operating layers

The same movement shows up in conduct rules. Japan's Financial Services Agency has published materials pointing toward a shift from Payment Services Act treatment to Financial Instruments and Exchange Act-style oversight for crypto-assets.

The working-group report recommends information provision, crypto-asset service-provider controls, market-abuse rules, insider-trading rules, SESC powers, and stronger user protection. The FSA's weekly review also notes draft Acts submitted to the Diet tied to FIEA and PSA amendments.

Japan's signal is about classification and conduct. Crypto assets are being pulled toward a framework where disclosure, surveillance, and misconduct rules shape participation. That makes access conditional on behavior, supervision, and accountability.

It also shows why regulatory design can be a form of infrastructure. Markets use law as a routing layer when participants need to know who can list assets, who can custody them, who can market them, and which forms of trading behavior create liability.

The UK is building a similar operating layer with a longer runway. The FCA says firms that want to carry on new regulated cryptoasset activities can apply from Sept. 30, 2026 to Feb. 28, 2027.

The new regime is expected to come into force on Oct. 25, 2027. A related consultation notice shows the regulator moving through authorization, supervision, consumer-duty, custody, prudential, and market-abuse work.

Europe already has the broader framework in place. ESMA says MiCA establishes uniform rules for crypto-assets covering transparency, disclosure, authorization, supervision, consumer information, market integrity, and financial stability.

A broader global regulatory map has already shown regulation moving as a multi-market process. The 2026 layer adds a sharper point: rulebooks are starting to decide how crypto products enter ordinary financial channels.

The UAE adds a payment-token example, but scope remains the constraint. The Central Bank's Payment Token Services Regulation provides the rulebook for payment-token activity, while a February CBUAE register provides a public check on licensed entities.

Separately, an ADX-hosted release says IHC, Sirius, and FAB received CBUAE approval to launch the dirham-backed DDSC on ADI Chain for institutional payments, settlement, treasury, and trade flows.

For now, the evidence points to a regulated payment-token framework and institutional settlement ambition; broad retail usage would need separate evidence.

South Korea adds a merchant layer. Crypto.com and KG Inicis said in March that they would integrate Crypto.com Pay across KG Inicis's merchant network for foreign travelers and K-commerce users, with merchants able to receive fiat or digital assets.

South Korea's K Bank partnership with Ripple points to another rail where bank and payments activity intersects with crypto. Both examples still need transaction data.

Their relevance is that they move the adoption debate toward checkout, settlement, remittance, and consumer-facing access.

Usage is the harder test

The US-centered interpretation remains powerful because the numbers are large. On April 29, total crypto market capitalization stood near $2.59 trillion, with Bitcoin around $1.56 trillion.

Dollar stablecoins still dominate the working liquidity layer, with Tether‘s 24-hour volume near $111.50 billion and USDC near $47.84 billion.

Those figures explain why US policy and dollar rails keep pulling attention. The dollar stablecoin system is already large. US capital markets supply legitimacy at scale.

The CLARITY Act stablecoin fight shows that the US debate is also about who captures the economics of digital dollars. That benchmark remains essential, because global crypto infrastructure still depends heavily on dollar liquidity.

Usage data complicates that benchmark. Chainalysis said adjusted stablecoin economic volume reached $28 trillion in 2025, with a baseline projection of $719 trillion by 2035 and a catalyst scenario approaching $1.5 quadrillion.

As projections, those figures are scenario math rather than proof of future payment flows. Their direction changes the operating question: stablecoins are being evaluated as payments infrastructure, treasury infrastructure, and settlement infrastructure, alongside their role as trading collateral.

The Chainalysis adoption work shows why emerging markets sit near the center of that debate. It ranked India first, followed by the US, Pakistan, Vietnam, and Brazil, and described adoption as broad-based across income brackets.

It also tied durable adoption to on-ramps, regulatory clarity, and financial and digital infrastructure. Those are the variables being tested by Pakistan's banking circular and by local-currency stablecoin efforts such as BILS.

The IMF adds the risk side. Its March paper on stablecoin inflows and FX spillovers finds that stablecoin flows can affect parity deviations, local currency depreciation, dollar premia, and financial stability.

Put simply, stablecoins become more consequential once they start behaving like a segment of the FX market.

That creates the live policy tension. Local-currency stablecoins can help keep domestic units relevant in on-chain finance. Banking access can pull VASPs into monitored channels.

Payment integrations can move crypto from portfolio exposure to checkout and settlement. Each rail also creates new supervisory demands around reserves, redemption, money laundering controls, market abuse, and currency pressure.

The evidence points to a specific split. US ETFs and Wall Street adoption have helped financialize crypto by improving access to exposure. The harder adoption test is happening where regulators decide whether crypto can touch local money, bank accounts, merchants, and FX markets.

That test is still early. BILS needs issuance and usage. Pakistan needs licensed VASPs operating through bank accounts. Hong Kong's new licensees need launches. Japan, the UK, and the EU need rules that work under market stress.

The UAE needs clean issuer and register mapping. South Korea needs merchant activity beyond announcements.

If those signals appear, the global crypto map will look less like a US-led investment-product cycle and more like a set of regional financial systems absorbing crypto under local rules. If they fail to appear, the dollar and US capital markets will keep doing most of the work.

The next test is usage, measured against attention.

The post Everyone is watching America’s crypto boom but Israel and Pakistan may be showing what comes next appeared first on CryptoSlate.