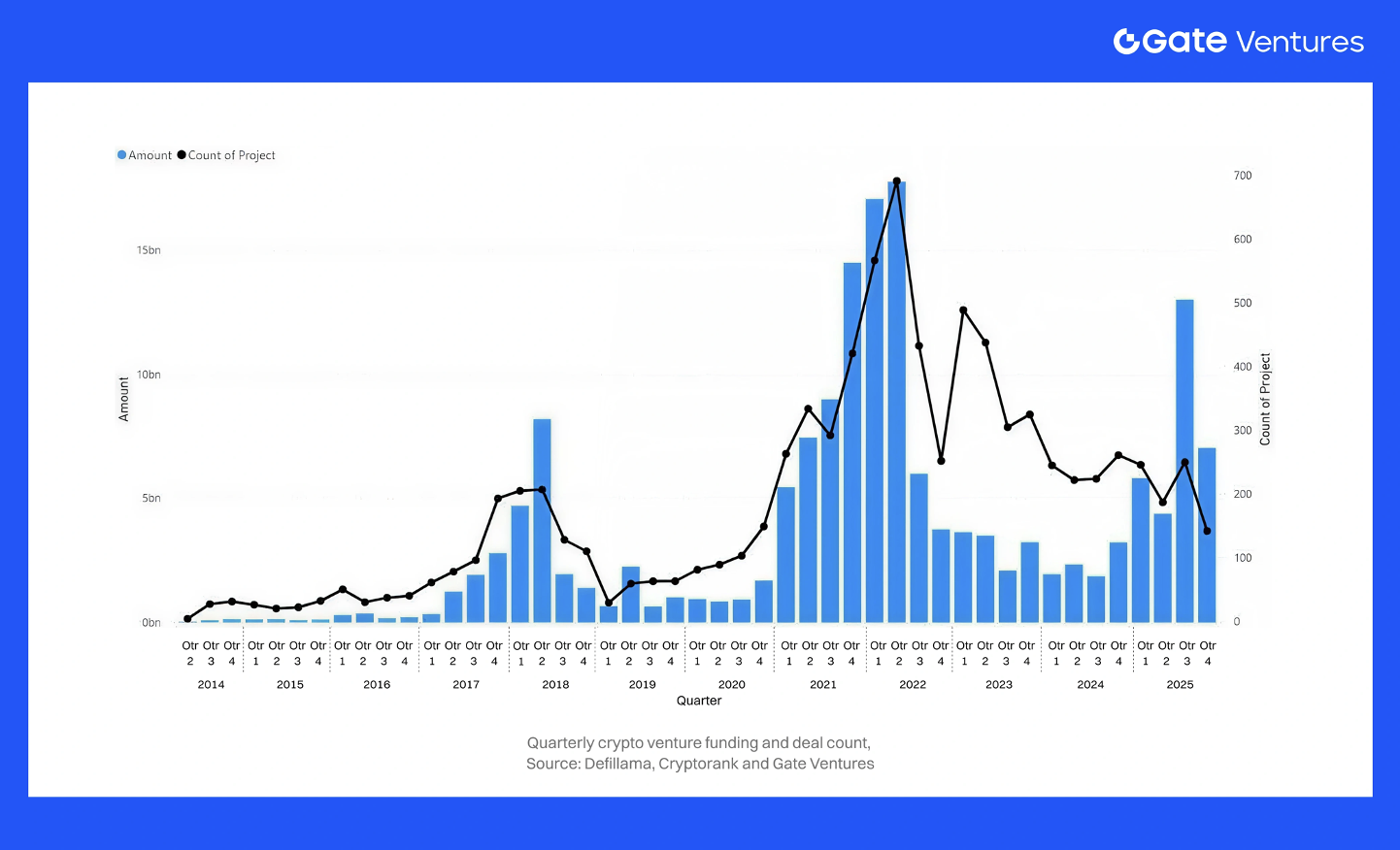

2025 wasn’t a “bull-market reset”—it was a quality-driven recapitalization. Funding surged to $30B+ YTD by Q4(with ~$13B in Q3) after the 2024 trough (~$9B), but deal count didn’t expand meaningfully, implying larger, more selective checks and a fat-tail headline.

Investors crowded into compliance-ready rails—payments/stablecoins/RWA, infrastructure, regulated trading, and info markets—while consumer narratives stayed lighter. Geography is turning multipolar, with clearer licensing hubs pulling weight outside the U.S. What matters next: where the new “default” institutional stack is forming—and who controls distribution in 2026

1. Total Capital Invested and Deal Count

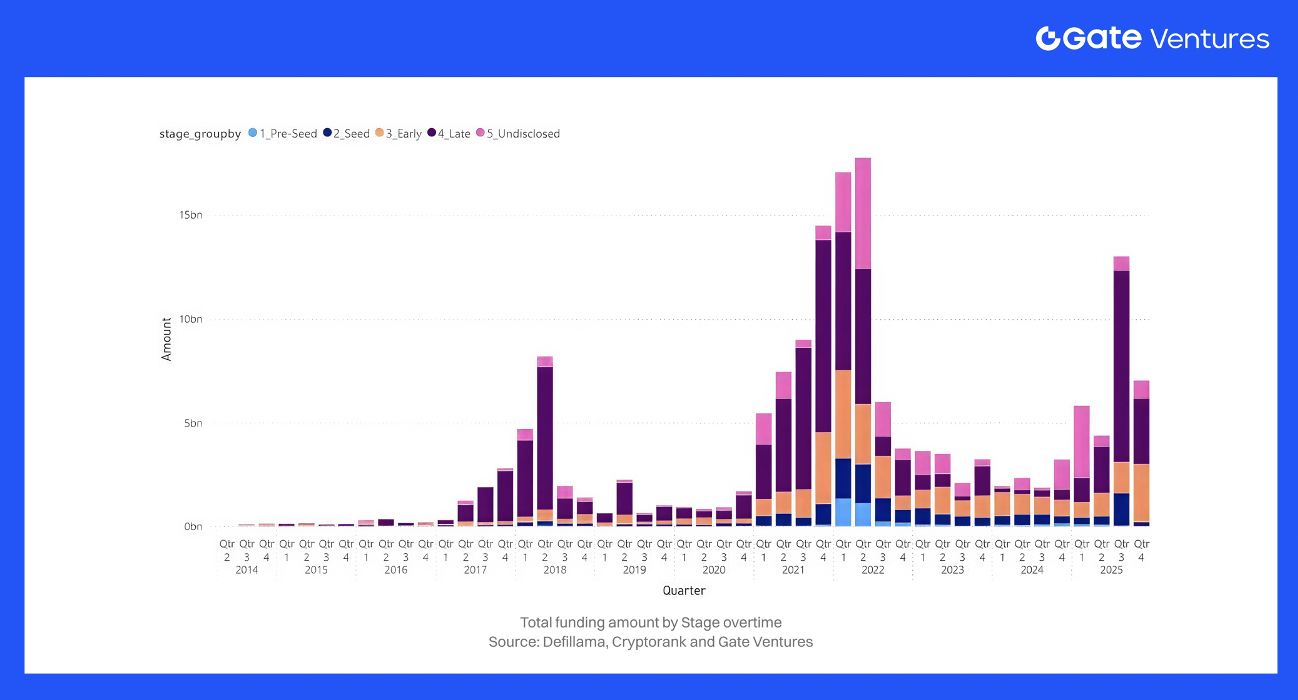

Crypto venture funding hit a cyclical low in 2023 and then rebounded strongly in 2024–2025.

In 2023, venture investors deployed roughly $12B into crypto startups – a –72% drop from 2022’s total as the frothy valuations of 2021–2022 gave way to bear-market caution. About 1,500+ deals were closed in 2023. In 2024, the market entered a clear trough. Total crypto VC investment fell to $9B in 2024 (-28% YoY decrease from 2023), and deal count fell slightly to ~952 deals for the year. Funding accelerated particularly in H2 2024 – for example, Q4 2024 saw $3.2B across 261 deals, a 46% jump in capital from Q3 despite a 13% drop in deal count as investors focused on larger bets.

2025 has been marked by a huge resurgence in capital deployment. By Q4 2025, year-to-date funding exceeded $30B, already surpassing 2024’s total by $21B. Quarterly investment hit multi-year highs – e.g. Q3 2025 alone saw ~$13B raised (the biggest quarter since Q1 2022). This was partly driven by a small number of mega-deals, which skewed aggregate averages but did not alter the underlying upward trend. Even so, the underlying trend is positive: excluding outliers, Q1–Q3 2025 funding was still roughly double the same period in 2024.

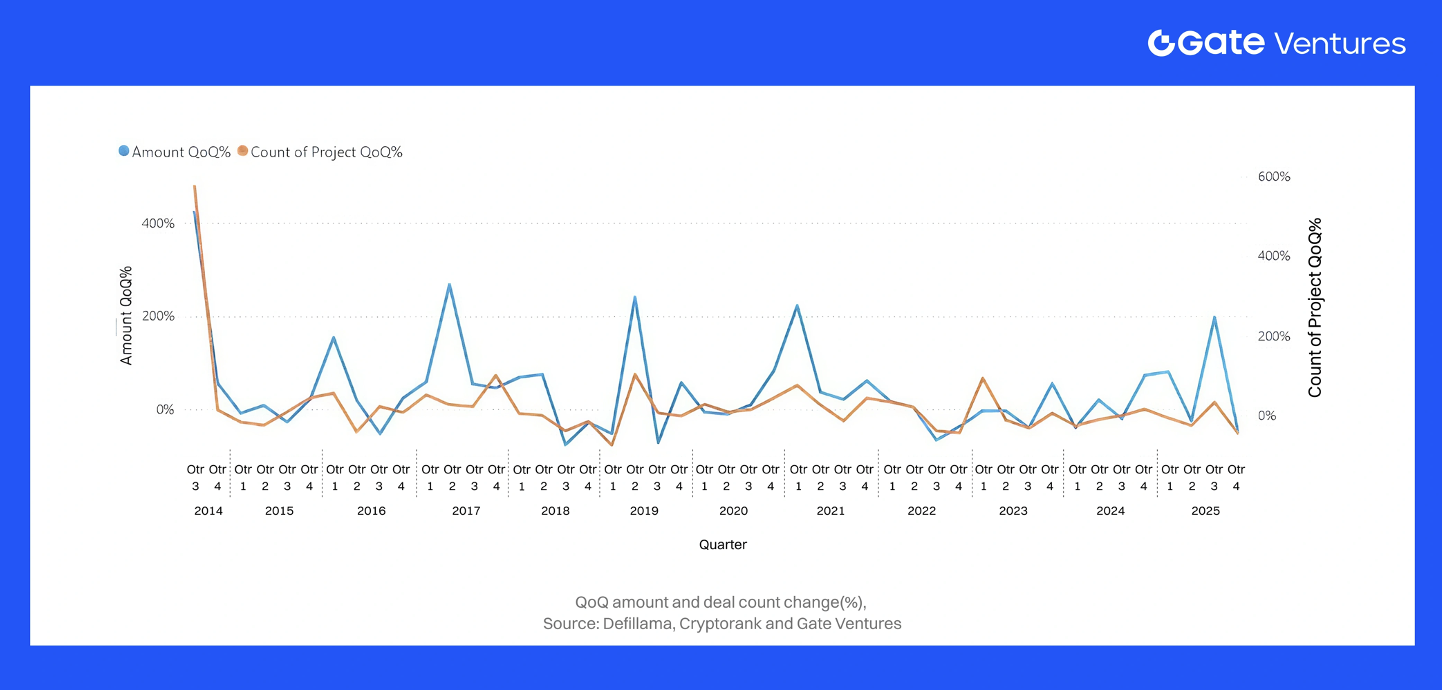

In contrast, deal counts in 2025 have not grown commensurately – in fact, some data suggests deal volumes may have stagnated or declined relative to 2024. For instance, there are ~800+ startup VC deals in 2025 YTD, down ~13%. The average deal size jumped as a result. In short, 2025’s increase in capital was driven by bigger checks rather than more startups funded.

Quarterly momentum: This momentum accelerated into H1 2025: Q1 2025 reached ~$4.8B (highest since Q3 2022), and although Q2 dipped to ~$2.0B (after the Binance boost in Q1), Q3 2025 rebounded ~+47% QoQ to $13B.

In other words, by mid-2025 the quarterly run-rate of crypto venture investment was back on par with early-2022 levels.

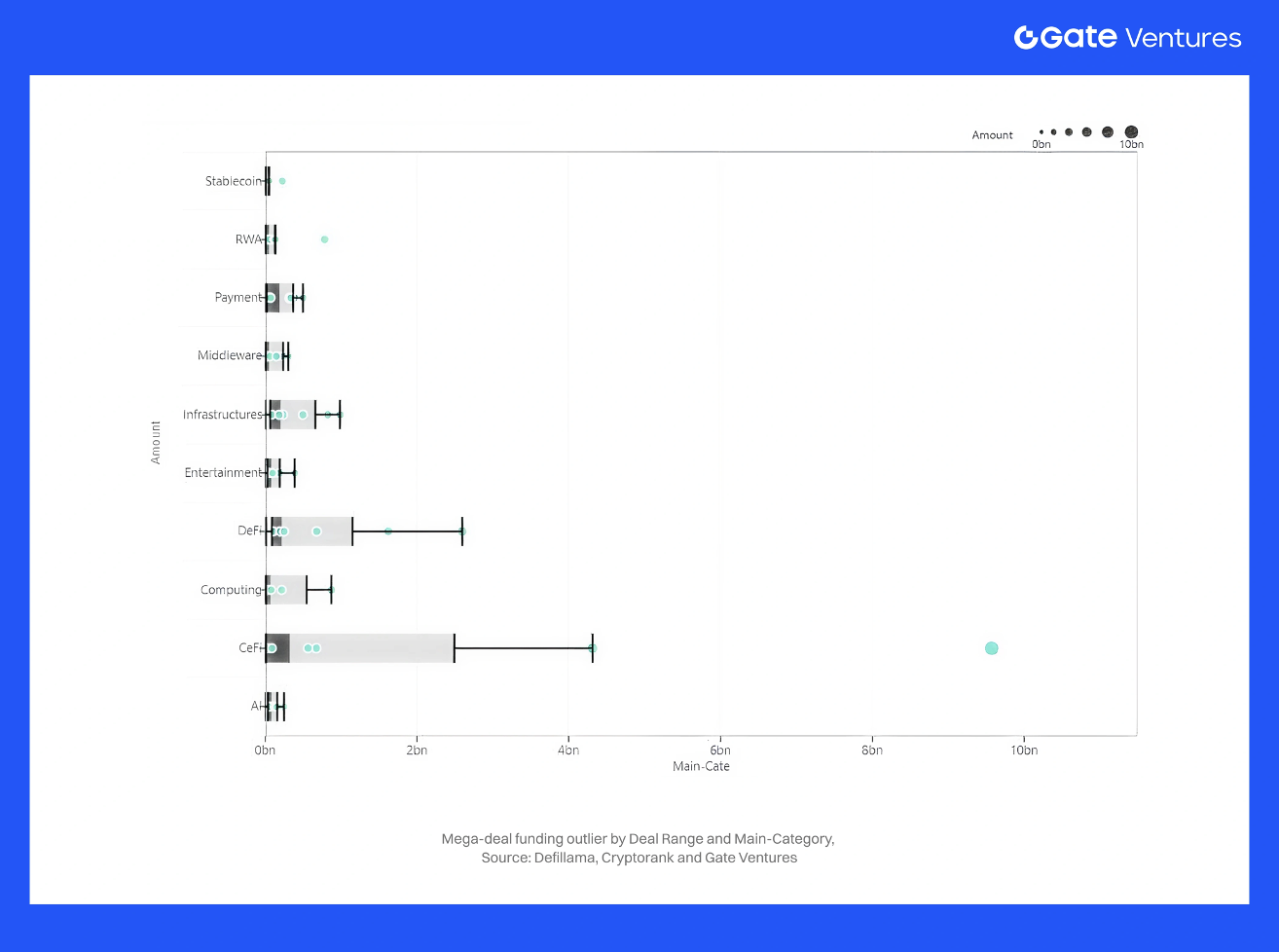

Mega-deals & skew on averages:

Mega-deals meaningfully distorted headline fundraising figures in 2025, creating a pronounced divergence between mean and median deal sizes. Binance’s $2B round in Q1 — the largest VC transaction in crypto history — accounted for ~34% of the quarter’s $5.8B total.

Late 2025 showed a similar pattern. Polymarket’s $2B raise and Kalshi’s $1B round (at an $11B valuation) will meaningfully inflate Q4 totals. The year also featured $300M for XY Miners, multiple $200M+ rounds across privacy, security, and infrastructure, and numerous $50M–$150M raises spanning L1s, L2s, and fintech. Additional outliers — including Ripple’s $500M strategic round and Bullish’s $1.11B IPO — contributed to a pronounced fat-tail distribution.

These mega-deals lifted average deal size, increased late-stage share, and widened the gap between mean and median. While highlighted for completeness, analysis of medians and ex-mega-deal trends is essential to reveal the underlying market: most deals remain small, even as a handful of ultra-large financings dominate aggregate capital.

Big-picture: Relative to the last cycle’s peak (2021–early 2022), current funding levels remain moderate. At the 2021 peak, crypto startups raised over $36B in a year (2021), fueled by a frenzy of seed deals and lofty valuations. 2022 saw over $44B (front-loaded before the market crash). In contrast, 2023’s ~$12B and 2024’s ~$9B indicate a reset to more sustainable levels.

The 2025 revival – on track to $30B+ – signals that the crypto venture market is climbing out of the winter, but with a very different character: more late-stage focus, more due diligence, and an emphasis on quality over quantity of deals. As we detail below, investors in 2025 gravitated toward certain sectors and stages, backing fewer but stronger projects, and positioning for what many expect to be a next growth cycle in 2026 and beyond.

2. Deal Size Distribution

The deal size distribution in 2023–2025 reflects a clear shift toward larger rounds. In 2024, deals under $10M accounted for over 75% of all activity, with the $5–10M bracket alone contributing ~76%. By contrast, in 2025 the < $10M share fell to ~61%, while most growth occurred in the $10–50M and $50M+ segments, producing a more pronounced barbell structure: early-stage activity concentrated in sub-$5M rounds, a thinner $1–5M middle, and a notable rise in large tickets at the upper end.

Several dynamics drove this shift:

- Stage correlation: Late-stage rounds accounted for ~45% of total capital (or deal count, specify, while early-stage rounds (Seed–Series A) remained mostly under $10M. By Q3 2025, ~10% of all deals exceeded $50M (vs. ~8% in 2024), signaling the return of large-check deployment.

- Category correlation: Mega-rounds clustered around CeFi and infrastructure — exchanges, brokers, and core blockchain systems frequently raised $100M+. Meanwhile, Entertainment and gaming/NFT projects remained in the lower brackets, typically sub-$5M.

- Investor correlation: Sub-$1M micro-rounds came primarily from angels and niche crypto funds, with fewer accelerator-led deals in 2025. Mega-rounds, in contrast, were led by large TradFi institutions and corporate VCs.

Overall, the market has bifurcated: most deals remain under $10M, but a small set of $50M+ and $100M+ rounds captures a disproportionate share of total capital, shaping the aggregate statistics despite representing a minority of transactions.

This comparison underscores the growing polarization in deal sizes – 2025 had relatively fewer mid-sized rounds and proportionally more very large rounds than prior years. For venture investors and startup founders, this means the fundraising market has become “go big or stay small”: substantial capital is available for top-performing later-stage projects, while early-stage teams face more competition for smaller checks.

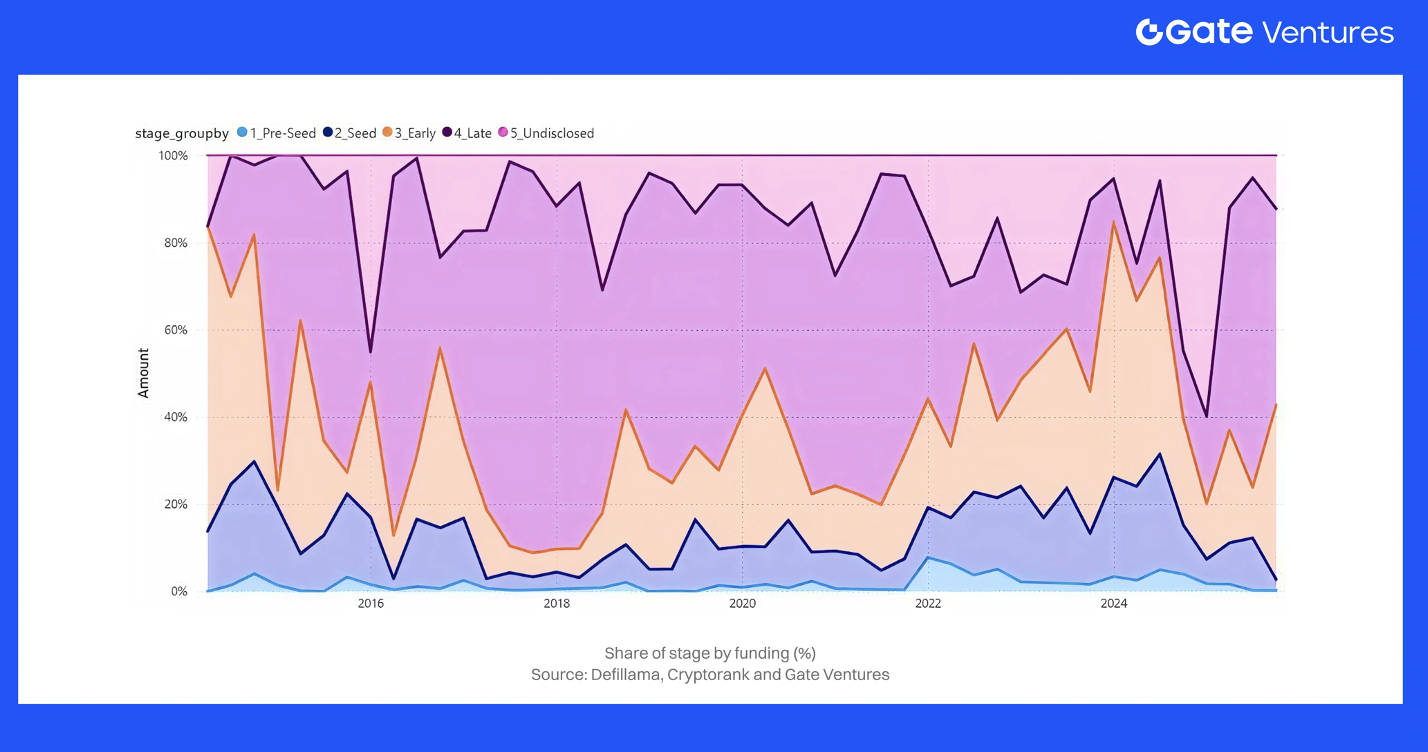

3. Fundraising by Stage (Pre-Seed, Seed, Early-Stage, Late Stage, Undisclosed)

Crypto funding stages shifted sharply from 2023 to 2025. In the 2022–23 downturn, late-stage rounds nearly vanished, leaving 2023 dominated by Pre-Seed, Seed, and occasional Series A deals. By mid-2025, the landscape reversed: Series B+ rounds captured the majority of total capital, while early-stage activity remained the core driver of deal count. As confidence returned, undisclosed-stage raises declined.

Pre-Seed

Pre-Seed deal share stayed surprisingly high in 2023–2024, even rising slightly in 2024—evidence of steady founder activity despite market stress. These rounds were very small in dollar terms, contributing only a few percent of total capital, often involving DAO grants or accelerator-style raises. Crypto-native funds continued backing pre-seed teams for low-cost optionality, keeping this pipeline consistently active.

Seed

Seed activity remained steady across 2023–2025 but with smaller checks than the 2021 cycle. Roughly 65% of 2023–2024 deals were under $5M, reflecting Seed/Seed+ norms. Median seed size gradually improved (~$2.5M → ~$3M), showing modest appetite recovery even as seed’s share of total capital fell with the return of larger rounds. In 2025, seed raises became somewhat easier but required stronger traction or technical proof, replacing the idea-stage momentum of 2021.

Early-stage (Strategic – Series A)

Early-stage was constrained in 2023, as few 2021–22 projects were healthy enough to raise full rounds. Conditions improved in 2024, with median early-stage rising ~26% to ~$4.8M and most rounds falling in the $10–50M range. By 2025, early-stage accelerated as bear-market builders matured. Many early-stage rounds—especially in infrastructure and DeFi—moved into the $10–50M range. Early-stage still dominated deal volume (>24% of all deals), but its share of total capital dropped to ~48%, overtaken by late-stage deployment.

Late Stage (Series B+)

Late-stage funding nearly vanished in 2022–2023, when post-unicorn failures pushed growth investors to the sidelines. Late-stage accounted for only ~10–15% of 2023 capital. Momentum returned in 2024: by Q4, Series B+ represented ~40% of quarterly capital. The full rebound arrived in 2025—over half of H1 2025 capital flowed into late-stage, though highly concentrated: a dozen to two dozen deals formed most of this 52% share. Early-stage remained high in volume, but late-stage rounds dominated dollars.

Undisclosed / Unknown Stage

In 2023, many companies avoided stage labels to mask down-rounds or bridge financings, creating a large “Undisclosed” category. As sentiment improved in 2024–2025, founders returned to standard labeling, reducing opacity. Strategic rounds—especially from exchanges—still appeared but were classified as late-stage due to size. Overall, 2025 featured far fewer undisclosed rounds, reflecting a healthier and more transparent market.

Stage Skew & Rationales

The stage rotation from 2023 to 2025 reflected clear market dynamics. In 2023, investors avoided late-stage risk, concentrating on early-stage rounds where valuations were low and bridge extensions could be raised discreetly. Late-stage funding fell to ~10–15% of total capital, and Series A/B compressed into small “extension” rounds.

As sentiment improved in 2024–2025, growth rounds reopened. By Q2 2025, 52% of capital flowed into later-stage deals, supported by regulatory clarity and stronger business fundamentals. Average late-stage check sizes remained stable ($6.4M → $6.3M from 2023 to 2024), while early-stage averages rose to $4.8M, signaling renewed confidence—before 2025’s mega-rounds pushed overall averages sharply higher.

Crucially, early-stage didn’t weaken. Crypto-native funds maintained pre-seed and seed activity through 2023–2024 and shifted to a barbell strategy in 2025: active pre-seed pipelines paired with concentrated late-stage deployment. Series A/B, thin in 2023, expanded again in 2025 as maturing bear-market builders returned to market.

In essence: 2023 = early-stage survival, 2024 = first late-stage rebound, 2025 = full late-stage comeback, with 2026 likely more balanced if macro conditions allow.

4. Fundraising by Categories (Main-Categories) & Sector (Sub-Categories)

4.1.Main Categories:

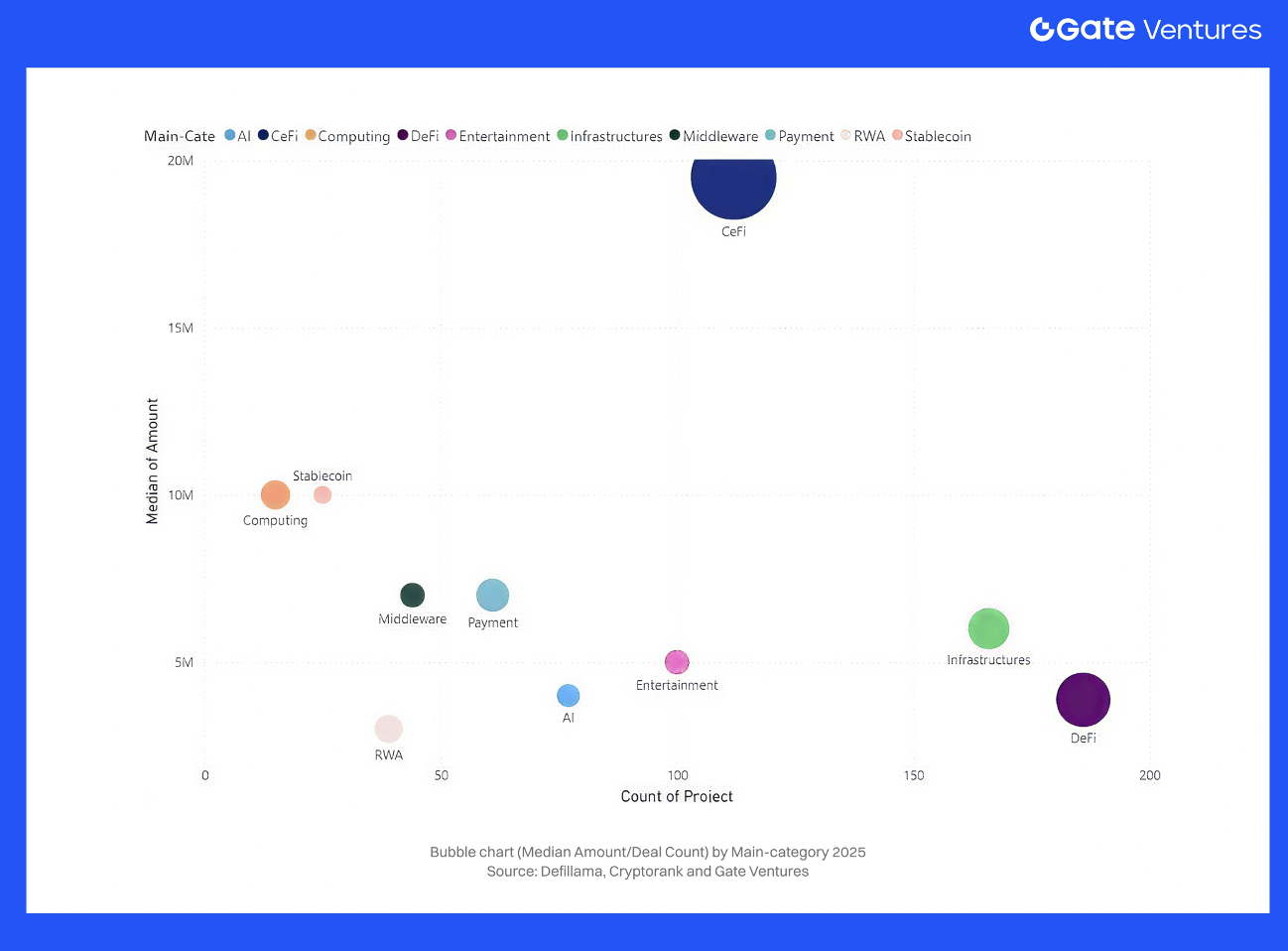

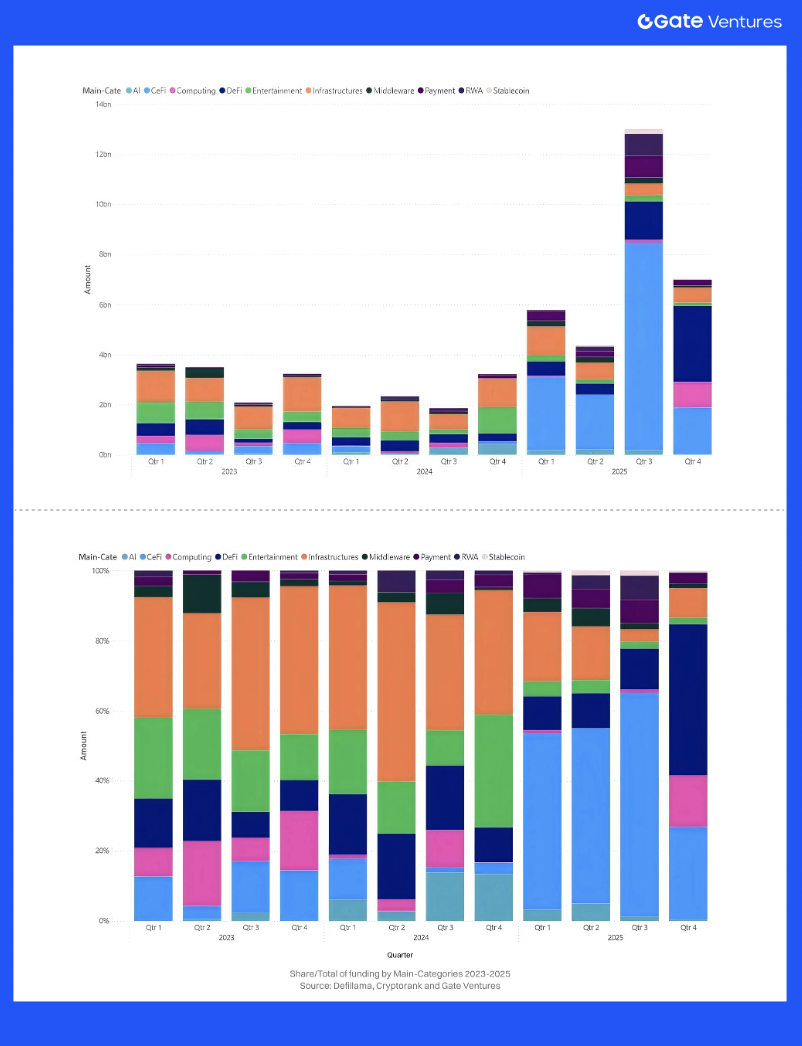

Over the past three years, investor sector preferences have rotated significantly, mirroring the changing narratives in crypto. In the 2021 bull, hot areas were DeFi protocols, NFTs/Gaming, and Web3 consumer apps, while by 2023–24 many of those fell out of favor, replaced by focus on core infrastructure, financial plumbing (stablecoins, custody), and new themes like real-world assets (RWA) or AI+crypto. The data shows clear shifts in which main categories (broad sectors) attracted the most capital in 2023 vs 2024 vs 2025:

CeFi

CeFi hit its post-FTX low point in 2023: most raises were distressed, sector share collapsed, and CeFi fell from 2021’s top-funded vertical to the bottom. A mild recovery began in 2024, led by regulated exchanges in Asia/Middle East and improving U.S. sentiment after the late-2024 pro-crypto Congress.

In 2025, CeFi re-entered the market with a few headline rounds, most notably Binance’s $2B raise, which significantly inflated H1 totals. Excluding this outlier, CeFi remained smaller than DeFi but clearly rebounding, with capital concentrating in compliance-aligned, institutional exchanges. Examples include EDX’s $85M raise (2023)during a weak market. Overall, CeFi bottomed in 2023 and began a gradual, regulation-driven recovery through 2024–2025.

DeFi

After the 2020–21 boom, DeFi cooled in 2022–23 as token prices fell, but remained a core category. 2023 funding centered on infrastructure-like DeFi (DEX aggregators, liquidity providers, risk tools) while speculative tokens faded.

Narratives shifted in 2024 toward real yield and TradFi integration, pushing DeFi/financial infrastructure to the top-funded category in several market reports.

Momentum accelerated in 2025: DeFi-related startups led all categories with $6.2B in H1, driven by stablecoin issuers, institutional DeFi, and financial infrastructure. Round sizes increased as institutional demand for compliance, revenue-generating protocols grew (derivatives, KYC pools).

DeFi dominated deal count in 2023–24 with small rounds; larger checks only returned in 2025—partly on the back of major stablecoin deals. Funds like Pantera, Dragonfly, and Multicoin remain bullish heading into 2026.

Infrastructure

Infrastructure was a top-funded category across 2023–2025. With application hype fading in 2023, capital rotated into L1s, L2 scaling, interoperability, dev tooling. Strength carried into 2024, where infra/Web3 saw +33.5% QoQ in Q4 2024, reaching $592M (16% of capital) across 53 deals, ranking #2 by capital and deal count.

H1 2025 accelerated further: L1/L2 ecosystems raised ~$3.3B, making infrastructure the second-largest category after DeFi.

Mining returned as a sub-sector: a $300M mining deal in Q2 2025 made “Mining” the top category that quarter, amplified by AI-driven compute demand.

Themes evolved each year — 2023: scalability/zk-rollups; 2024: modular/app-chains; 2025: identity, compliance, real-world integrations.

Infrastructure consistently captured large round sizes, high valuations, and remained foundational heading into 2026.

Payments & Stablecoins

Payments and stablecoins became a standout category from 2023–2025 as real-world utility took center stage. After the 2022 fallout, stablecoins proved the most scalable use case: by Q4 2024, stablecoin businesses captured 17.5% of total funding, boosted by Tether’s major raise.

Capital then expanded toward asset-backed stablecoins, payment rails, cross-border infra (e.g., Circle’s Elements acquisition, Ripple’s ecosystem investments). In H1 2025, stablecoin/payment networks pulled in ~$1.5B, reflecting rising adoption and yield-driven demand. VCs backed wallets with embedded payments, merchant integration, compliant processors, and emerging-market issuers.

AI x Crypto

AI–crypto convergence emerged as a real narrative from 2023–2025. Early rounds in 2023 were small (Fetch.ai, SingularityNET, a handful of seed-stage entrants).

By 2024, AI+blockchain gained traction but remained minor. Small checks went to ChainGPT, AI marketplaces, and decentralized compute.

The category broke out in early 2025 with ~$0.7B raised, its first meaningful capital cycle. Notable deals included Gensyn’s $43M (decentralized compute) and multiple AI-driven trading/security platforms.

While retail chased 2024’s meme-AI tokens, VC capital focused on compute, automation, agentic systems, and early infrastructure for decentralized AI. By 2025, AI+crypto grew from near-zero (2022) to a credible niche (~$700M), positioned for stronger expansion in 2026.

RWA (Real-World Assets) & Tokenization

RWA tokenization became a top cross-sector narrative by 2024–2025.

2023 activity was early: Maple Finance pivoted to RWA lending; several pilot programs emerged. Momentum grew in 2024, with projects raising to tokenize bonds, treasuries, ETFs (Ondo’s $10M, Matrixdock, Backed Finance).

By 2025, RWA became a core venture theme and a major driver within DeFi/financial infra. Much of H1 2025’s $6.2B DeFi/Infra funding came from RWA-aligned startups: stablecoin issuers, tokenized funds, compliant lending pools, and yield products backed by real collateral.

Though datasets rarely separate RWA as a standalone category, it became one of the fastest-growing, institution-ready verticals entering 2026.

Middleware & Others

Middleware (developer APIs, indexers, compliance tools) remained smaller but steady from 2023–2025. Security/compliance startups attracted ~$1.2B in H1 2025, driven by enterprise demand and regulatory requirements. Developer infra (compute/storage: Filecoin ecosystem, Akash, etc.) saw moderate traction.

Social/Web3 Social had isolated wins (Farcaster’s $30M, friend.tech clones) but lacked broad PMF, keeping deal share limited.

Entertainment (Web3 Social, NFTs, Gaming)

Once leading categories in 2021, NFTs/gaming collapsed in 2023 as hype evaporated. Throughout 2023–24, most VCs avoided the sector; reports noted gaming/metaverse/NFTs “failed to capture significant attention.”

However, Q4 2024 showed a misleading spike: Web3/NFT/Gaming became #1 by deal count (22%) and reached ~$771M (21% of capital) almost entirely due to Praxis’s $525M mega-round.

In H1 2025, the sector returned to baseline with ~$0.6B (~5% of total)—mostly early-stage. Many teams pursued token raises instead of equity, further reducing VC visibility. By 2025, interest ticked up slightly (better-quality games, stronger NFT infra), but mainstream VCs remained cautious. High deal count, low capital share: a classic “prove-it” phase.

Category trends show a clear rotation across cycles:

- 2023: Infrastructure and middleware dominated the sparse funding landscape as investors avoided consumer apps.

- 2024: Stablecoins and financial infrastructure surged, Infrastructure and Web3 held secondary positions, while entertainment sectors remained quiet.

- 2025: “Serious” verticals—DeFi (particularly RWA/stablecoin) and Infrastructure (L1/L2)—captured nearly 75% of all H1 2025 funding, while Entertainment (NFTs/Gaming) slid to <5%. AI, RWA, and Security/Compliance became meaningful contributors.

- Despite capital concentration in a few power categories, the investable universe broadened. More segments—privacy, identity, AI, decentralized physical networks—attracted funding compared to 2019–20, showing a maturing, more diversified crypto VC landscape.

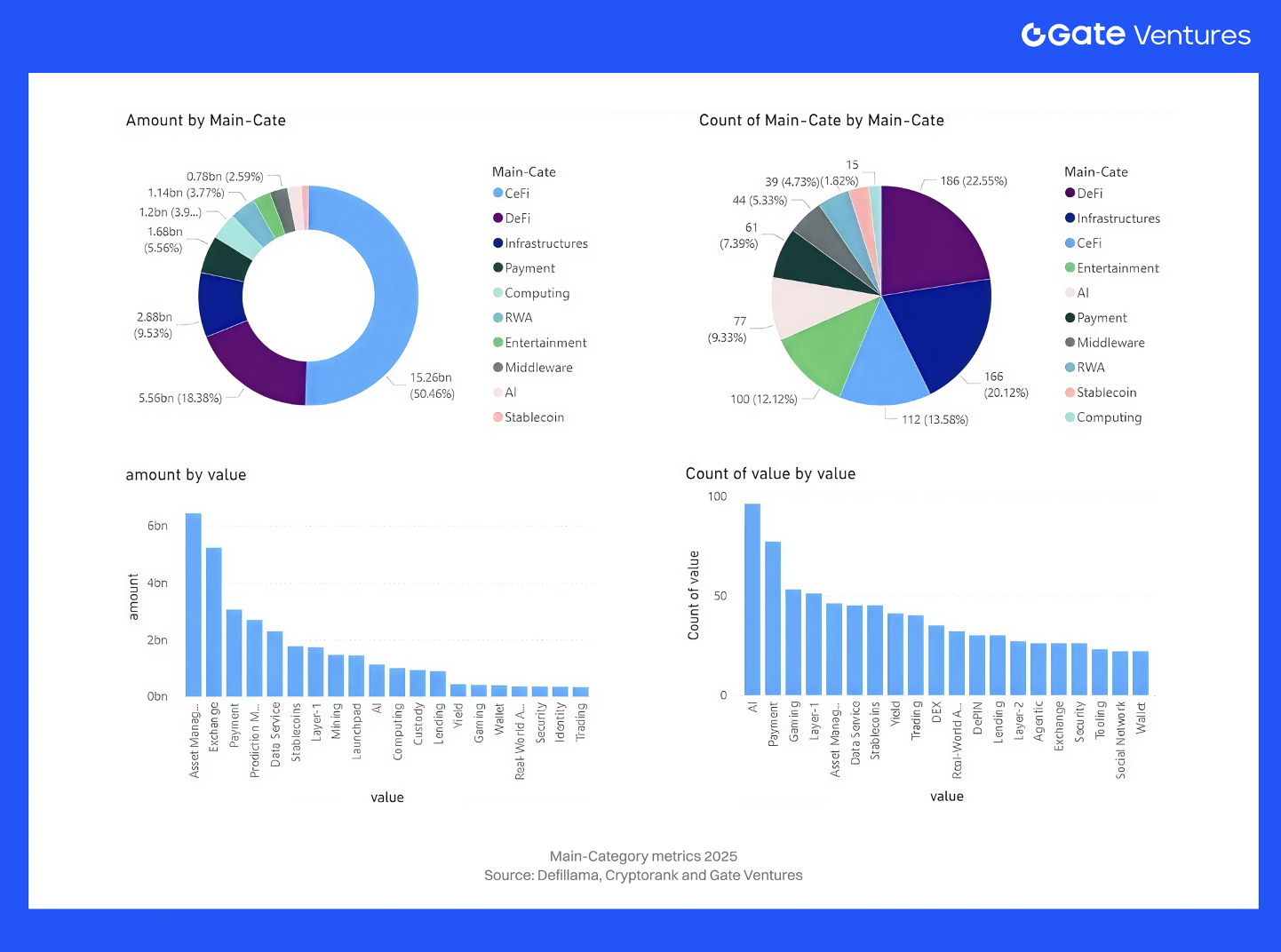

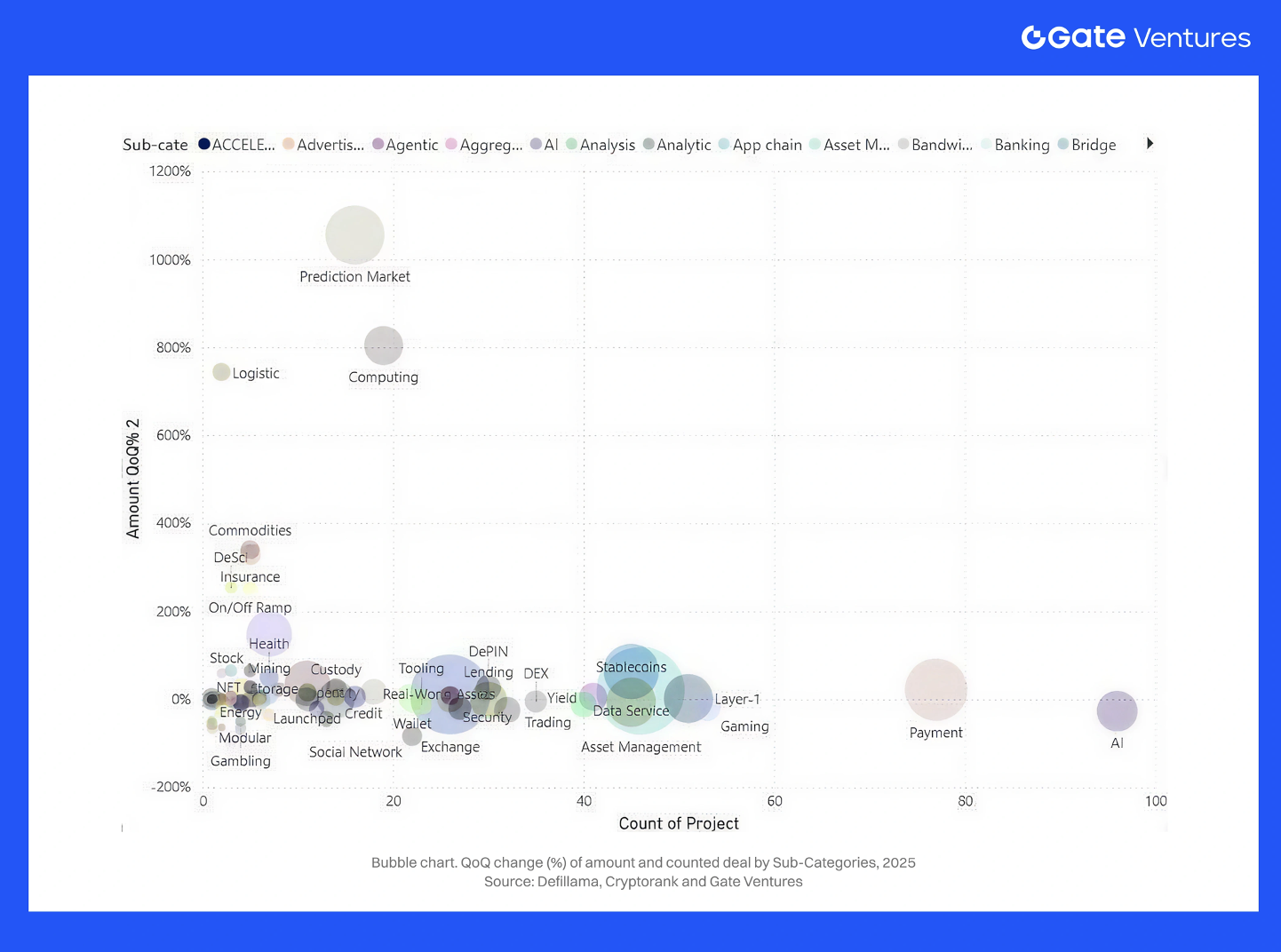

4.2. Sub-Categories and Emerging Narratives

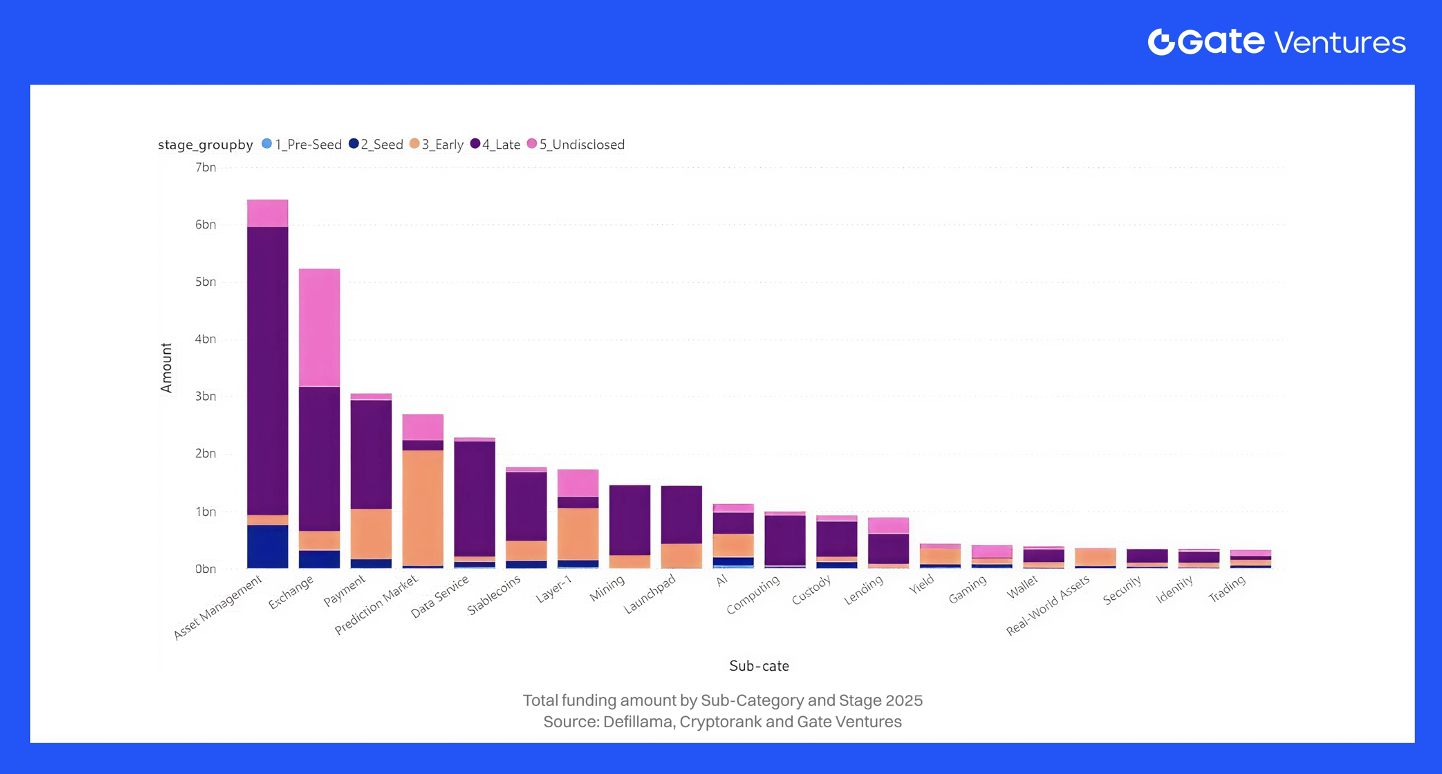

Sub-sector flows from 2023–2025 show capital clustering around a handful of dominant narratives rather than evenly across the market. Across the 20 largest verticals, roughly $33.5B was raised from 2023–2025, with just five categories—Exchanges, Asset Management, Payments, Layer-1, and Prediction Markets—absorbing ~53%. Funding fell from ~$6.1B (2023) to $3.6B (2024) before surging to $20B in 2025 as late-stage and mega-rounds returned.

Exchanges, Launchpads & Trading

Exchange funding vanished in 2023–24 post-FTX, with almost no fresh capital until 2025. The reversal was dramatic: Exchanges raised ~$5.1B in 2025 alone, ~87% in late or undisclosed rounds. Launchpads and trading venues added another ~$2.0B across 2023–25, with $1.5B+ in 2025, mostly late-stage ($50–100M+).

Together, the broader trading stack (Exchange + Launchpad + Trading + Data) grew from $0.6B (2023) and $0.4B (2024) to ~$7.8B in 2025, driven by recapitalization of licensed CEXs, token-launch infra, and market-data providers. By 2025, investors were again funding centralized liquidity hubs—only when paired with licensing and compliance.

Asset Management, Custody, Yield & RWA

Asset Management was the #2 sub-category, raising ~$4.35B in 2023–25, with ~$3.8B in 2025 alone. About 60% of this was late-stage, reflecting scaled managers building CeDeFi/RWA portfolios; another 20% remained Seed-stage, showing continued creation of new managers.

Custody added ~$0.48B, Yield protocols ~$0.27B, and RWA platforms ~$0.62B with a balanced Early/Late mix.

This cluster raised ~$1.3B (2023) → $0.5B (2024) → ~$4.6B (2025) as tokenized treasuries, credit funds, and yield-bearing stablecoins moved from pilot testing to distribution.

Investors increasingly view asset managers + custody + RWA rails as a single structural bet on institutional on-chain portfolios.

Security, Custody, Lending & Credit

- Security/compliance middleware remained essential, raising ~$0.49B (2023–25), with ~47% Late-stage and ~23% Early, re-accelerating in 2025 (~$0.25B) amid rising hacks and AML demands. Custody (as above) skewed heavily Late-stage (~70%), reflecting consolidation around institutional-grade providers.

- Lending/credit raised ~$0.73B: $0.24B (2023) → $0.16B (2024) → $0.33B (2025). Stage mix was unusual—~13% Late, ~35% Early, ~37% Undisclosed—consistent with the sector rebuilding after 2022 CeFi failures and focusing on RWA-backed or under-collateralized credit experiments over large growth rounds.

Payments, Stablecoins & Data Services

- These became core infrastructure categories. Payments raised ~$3.0B across 2023–25, with $2.3B in 2025, ~63% Late-stage—appropriate given regulatory + liquidity requirements. Stablecoin platforms added ~$1.9B, rising from near-zero (2023) to ~$1.65B (2025), again Late-stage heavy.

- Data Services raised ~$1.7B, >65% Late-stage, with $1.2B in 2025, underscoring how analytics, oracles, and risk engines now underpin payments, credit, and RWA issuance.

- Together, Payments + Stablecoins + Data grew from ~$0.7B (2023) to ~$5.2B (2025)—clear evidence that the market is now funding value-transfer + information-transfer rails, not just trading venues.

Prediction Markets & InfoFi

- A breakout story of 2025. Prediction markets raised ~$2.68B across 2023–25—all of it in 2025.

About 75% of volume was Early-stage, with the rest Late/Undisclosed, reflecting one or two ultra-mega rounds (>$500M) into regulated Kalshi-style exchanges plus a long tail of early InfoFi (markets for signals, labels, research). - Prediction markets evolved from niche betting to information infrastructure underpinning pricing for macro, credit, and governance risk—hence renewed VC conviction.

Layer-1, Mining, Computing & Infrastructure

- Layer-1 chains raised ~$2.71B (2023–25): $0.65B (2023) → $0.75B (2024) → ~$1.3B (2025). Nearly 48% of L1 capital was Early-stage; ~25% was Late/Undisclosed. Investors still back new execution environments but expect faster ecosystem delivery.

- Mining/compute infra raised ~$2.38B: $1.1B (2023) → ~0 (2024) → ~$1.28B (2025). About 74% of mining capital was Late-stage, reflecting industrial-scale BTC mining, energy, and sovereign/infrastructure investors.

- Pure “Computing/DePIN GPU networks” remained small (~$50M), mostly Seed/Early, indicating an emerging but not yet scaled storyline.

AI, Gaming, Wallets & Consumer UX

- AI was the most active sub-category by deal count: 30+ deals (2023) → 40+ (2024) → ~70 (2025), totaling ~$2.0B. Stage mix: 20% Seed, 33% Early, 25% Late, 20% Undisclosed—a full pipeline from agentic infra to later-stage platforms.

- Gaming raised ~$1.54B (2023–25), declining from $0.74B (2023) to $0.42B (2024) and $0.38B (2025)—mostly Seed/Early with high Undisclosed share. Wallets raised ~$0.94B, front-loaded in 2023 with dips in 2024 and modest rebound in 2025. Identity tooling brought ~$0.45B, spread across stages.

- Consumer UX no longer drives the cycle; instead, identity, key management, and AI copilots are quietly gaining traction. Privacy funding remained steady (e.g., Aztec’s $100M plus multiple early ZK infra raises).

Combined custody/security/compliance reached $1.2B by 2025, reflecting surging institutional demand for compliance rails.

4.3. Conclusion

The sub-category view reinforces the core shape of the 2025 cycle: capital concentrated heavily in regulated exchanges, asset managers, payments and stablecoin rails, prediction markets, and heavy infrastructure (L1, mining, data). These sectors absorbed most late-stage and mega-deal volume, while AI, identity, and InfoFi remained early- and mid-stage bets on a more automated, data-driven financial stack. Consumer categories—gaming, NFTs, SocialFi—persisted but no longer defined the cap table.

The market has clearly bifurcated. High-conviction, revenue-anchored verticals—stablecoins/RWA, L1/L2 infra, exchange infra, compliance/security—pulled the largest checks, while speculative narratives from the 2021 cycle attracted only selective funding. Capital has shifted from hype to functional, regulated, and institution-ready infrastructure.

As 2026 approaches, the test is whether these newly funded rails—payments, stablecoins, RWA platforms, prediction markets, compliant CEX/CeDeFi venues—convert into sustained transaction volume and fee revenue. Investors increasingly expect deeper real-world integration, continued scaling of core infra, and more mature AI convergence, with certain ecosystems (e.g., Solana) well-positioned to benefit. The narrative has moved decisively toward utilitarian, foundational crypto infrastructure.

5. Fundraising by Geography

The geographic distribution of crypto venture funding became more diverse from 2023 to 2025, although the United States remains the single biggest locus of investment. We observe a slight decentralization of deal activity away from the US, driven by regulatory uncertainty there and proactive crypto initiatives in other countries. Key regional trends include:

United States

The US remains the largest crypto-VC hub, though its dominance is gradually easing. Despite regulatory pressure, US startups captured 30%+ of global activity in 2023, ~24% of deals. In 2024, and ~25% of capital and ~36% of deals Q4 2024.

In 2025, the US accounted for 31% of capital and 41% of deal count.

A temporary dip in Q1 2025 occurred only because Binance’s $2B Malta-based raise skewed global totals.

Going forward, the US should remain the largest market in absolute terms—supported by ETF inflows and clearer laws—but its share is likely to drift slowly downward as Asia and Europe accelerate.

Asia (Singapore, Hong Kong, Japan, Korea)

Asia’s footprint expanded sharply from 2023–2025:

- Singapore: consistently top-3 by deal count (~9% in Q4 2024, 6.4% in Q2 2025) with stable capital share (~3–4%).

- Hong Kong: surged after launching its licensing regime, capturing 17% of global capital in Q4 2024—second only to the US; despite small deal count (~2–3%), reflecting large outlier rounds such as HashKey’s $500M.

- Japan: ranked #3 globally by capital (~4.3% in Q2 2025) driven by major corporate blockchain initiatives.

- South Korea: highly active in gaming/consumer crypto.

By 2025, Asia collectively represents ~20–30% of global crypto VC funding—up from ~10–15% just a few years earlier—driven by rising CeFi hubs, gaming ecosystems, and funds such as Fenbushi, HashKey, and Yzi Labs.

Europe (UK, EU)

Europe gained strong momentum after MiCA, offering rare regulatory clarity.

- The UK captured 22.9% of global capital in Q2 2025, second only to the US, and ranked #2 by deal count (~8%), supported by London’s push to become a crypto hub.

- Across the EU, multiple hubs strengthened:

- France (Binance EU HQ, Ledger’s $100M raise)

- Switzerland (~3.7% of Q2 2025 deals; foundation base for major L1s)

- Germany (regulated crypto financial products)

- Portugal (founder-friendly)

Europe now claims a meaningful and rising share of global VC flows, hosting major DeFi teams (e.g., Aave) and frequent Series A/B raises. With MiCA fully active from 2024 onward, the region is positioned for continued growth.

Middle East & Other Regions

The Middle East is emerging quickly as a crypto-friendly capital hub. The UAE continues attracting exchanges and Web3 teams, supported by sovereign wealth funds. A notable example: Abu Dhabi led a $250M round for Rain in 2023. Regional share remains <5%, but is rising.

Latin America and Africa show strong retail adoption but smaller VC volumes; ongoing seed rounds focus on remittances and fintech (Ripple, Bitso, YellowCard). Some teams operate in “Global/Remote-first” mode, reducing geographic attribution.

Undisclosed Geography

A subset of rounds remains geographically unspecified—DAOs, remote teams, or stealth projects. As regulations tightened across 2023–2025, fewer teams stayed jurisdiction-less; many adopted hubs like Singapore, BVI, UAE for clarity.

Conclusion

By 2025, crypto VC allocation is clearly becoming multipolar.

- The US remains the largest hub, but slowly declining in global share.

- Asia (Singapore/HK/Japan) and Europe (UK/Switzerland/EU) have significantly increased both deal count and capital.

- Geographic concentration is easing, reflecting the global nature of the ecosystem.

- If current trends hold, 2026 could show a more balanced distribution hypothetically: US ~40%, Asia ~30%, Europe ~20%, Others ~10%, as increasingly geography-agnostic investors fund teams worldwide.

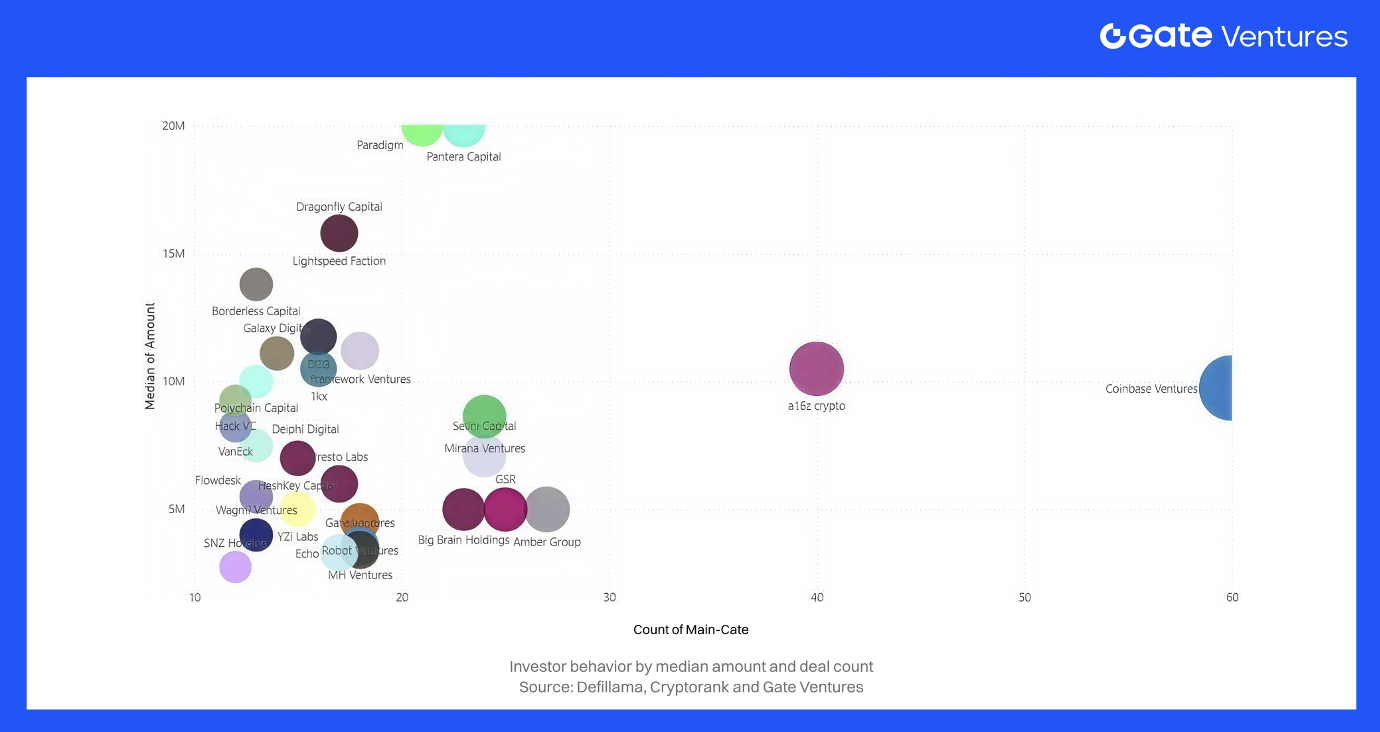

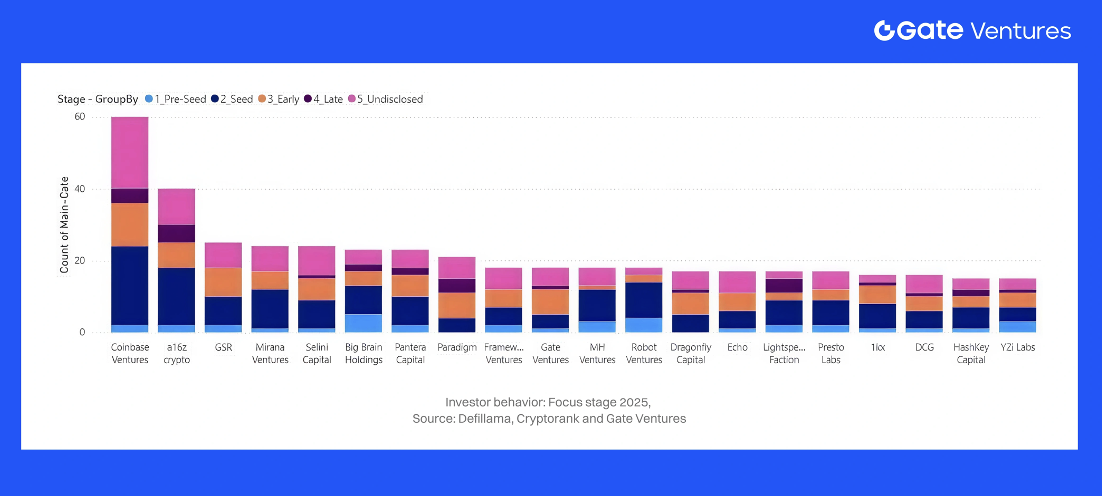

6. Investor Behavior and Top Investors (2023–2025)

Investor Behavior (2023–2025): Who Is Actually Deploying Capital?

Market Structure: Fewer Funds, More Concentrated Investment

Between 2021 and 2024, the number of active US venture firms fell by more than 25% (from ~8,300 to ~6,200), as limited partners concentrated commitments into a handful of large franchises. Financial Times, Crypto VC followed the same pattern: overall funding volumes recovered from the 2022–2023 trough, but with capital increasingly concentrated in a small core of repeat crypto-native and crossover investors.

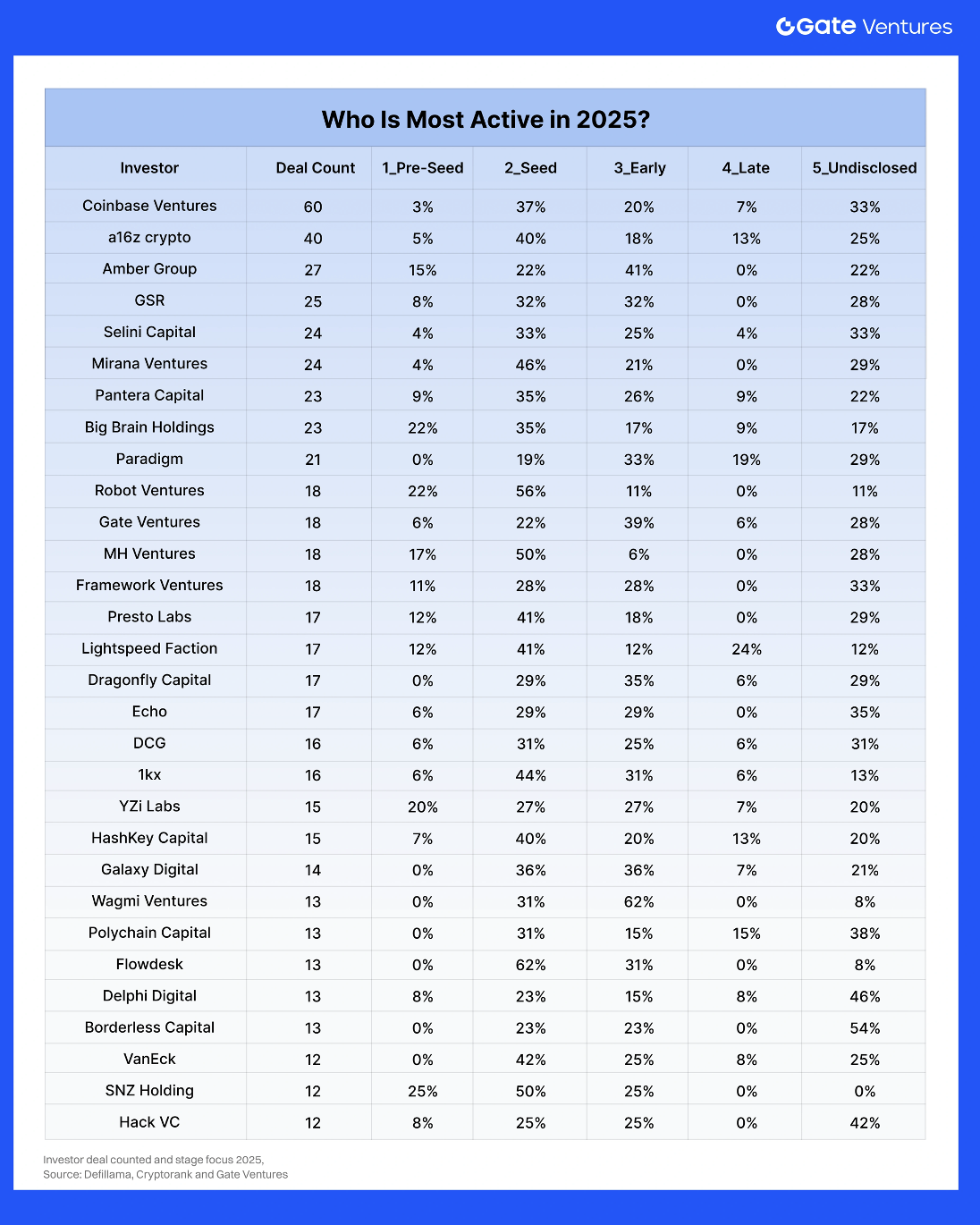

Inside that tighter market, the top investors in Q3 2025, capturing ~32% of all 2025 YTD transactions. Coinbase Ventures led with ~60 deals in 9 months of 2025, cementing its position as the most active fund. Meanwhile, the 2021-era “tourist investors” have vanished — 2025 belongs to specialized, multi-cycle crypto VCs with real conviction.

Who Is Most Active in 2025?

This table highlights three key facts relevant for 2025:

- Coinbase Ventures, Big Brain Holdings, and Yzi Labs (Binance Labs) are extremely active in volume, particularly at early stage.

- Pantera, Polychain, Paradigm, Dragonfly, Multicoin, Framework form the “heavyweight” belt: multi-fund platforms with a long track record and high lead ratio, able to write larger checks at Series A+ and growth.

Putting dataset and public rankings together, 2025’s most active investor cohort is effectively:

- Early-stage ecosystem amplifiers: Coinbase Ventures, Big Brain Holdings, 1kx, YZi Labs, plus chain-ecosystem funds (Solana Ventures, Polygon, etc.).

- Full-stack crypto VCs: a16z crypto, Paradigm, Polychain, Pantera, Dragonfly, Multicoin, Framework, Gate Ventures.

- Strategic corporate/TradFi entrants: bank-backed or corporate vehicles (Standard Chartered/JV, payment companies, fintechs) selectively joining later-stage or strategically important deals.

Stage Behavior: From Early-Stage Dominance to a Barbell Market

By 2025, the pattern reversed. Funding reached $4.59B across 414 deals, with late-stage capturing ~56% of capital and early-stage ~44%. Q2 2025 alone recorded 31 rounds over $50M, while sub-$1M checks declined—signaling bigger tickets and a more selective, mature market.

The Stage Shift

2023–2024:

- Seed/A dominated

- Many tiny rounds (<$1M)

- Minimal growth capital

2025: A clear barbell pattern:

- Top early-stage funds (Coinbase Ventures, Big Brain, 1kx, YZi Labs, Framework, Pantera) continued backing pre-seed/seed

- Growth capital returned aggressively to CeFi, RWA, trading infra, and L1/L2 with $50–$500M+ rounds

Dataset reflects the same structure: in 9 months of 2025, early-stage still accounts for 60%+ of deal count, but late-stage captures ~37–40% of capital (up from mid-teens in 2023–24). Q3 was further boosted by mega-deals in exchanges, mining/AI compute, and regulated prediction markets—often involving TradFi and sovereign funds.

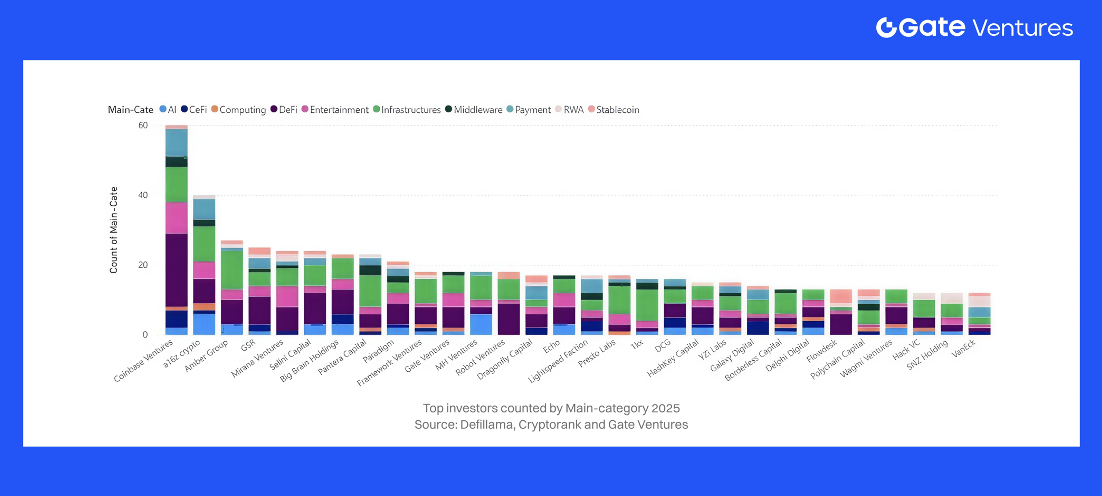

Sector & Thesis Biases: Who Backs What?

Across 2023–2025, sector preferences of leading investors converged around a few structural narratives:

- Trading, CeFi & CeDeFi

Trading and CeFi/CeDeFi remained dominant, pulling in ~$2.1B of the $4.59B raised in the reference quarter. Mega-rounds included Binance’s $2B, Revolut’s $1B, and Kraken’s $500M, backed by multi-cycle giants such as Pantera, Paradigm, Polychain, and Dragonfly, alongside corporate and sovereign co-investors.

Gate’s dataset shows similar patterns: CeFi/trading is a core focus for Binance, YZi Labs, Coinbase Ventures, and OKX Ventures, who deploy strategically to strengthen exchange ecosystems and liquidity networks.

- DeFi, On-Chain Credit & Structured Yield

Top crypto-native funds — 1kx, Framework, Polychain, Dragonfly, Pantera, Multicoin — remained deeply committed to DeFi: perps, restaking, RWAs, and credit. These investors not only provide early capital but often help shape token and governance architecture, effectively designing the emerging on-chain financial system.

- Infrastructure, ZK & Interoperability

Paradigm, a16z crypto, Polychain, Gate Ventures, and Dragonfly continued to anchor L1/L2, ZK, data availability, and interop investments. After quieter deployment in 2023–2024, they returned in 2025 with high-conviction infra bets — advanced ZK systems, AI-driven protocols, interoperability layers, and regulated synthetic/prediction markets — sectors where technical and regulatory complexity create strong moats.

- RWA, CeDeFi & Tokenized Yield

Pantera, Framework, 1kx, Polychain, Dragonfly, and bank-adjacent strategics increasingly targeted RWA issuers, CeDeFi managers, tokenized T-bills, credit funds, and yield-bearing stablecoins. These verticals accelerated from 2024 into 2025, reflecting institutional appetite for compliant, yield-generating on-chain products that bridge Web2 and Web3.

- AI x Crypto, Consumer, Gaming

Coinbase Ventures, Big Brain Holdings, and similar early-stage specialists anchored the consumer/gaming/AI lane, especially across Solana. Their focus blends consumer UX, agentic AI systems, Web3 tooling, and early InfoFi/prediction use cases — areas with high experimentation but comparatively smaller tickets than infra or CeFi.

2025 vs 2023–2024: How Has Investor Behavior Actually Shifted?

Concentration vs dispersion:

2021–22 saw hundreds of generalist funds flooding crypto. By 2023–24, funding recovered modestly ($10.1B → $13.6B), but most generalists exited. In 2025, H1 alone surpasses $16B, the market consolidating around ~30–50 crypto-native funds (Coinbase Ventures, YZi Labs, Big Brain, 1kx, Polychain, Pantera, Dragonfly, Multicoin, Gate Ventures, Framework) controlling a large share of deal flow.

Stage mix: In 2023–24, early-stage dominated: 85% of capital in early rounds and just 15% in late-stage. In 2025, late-stage returns aggressively shows 56% of capital going to later-stage rounds, driving mega-deals in trading, CeFi, mining/AI infra, and regulated markets.

Sector tilt:

- 2023: Infra, DeFi, L2s lead as the ecosystem rebuilds post-FTX.

- 2024: RWA, restaking, infra remain strong; early on-chain credit + AI x crypto show up in seed portfolios

- 2025: Allocations shift to trading/CeFi, CeDeFi managers, RWA, on-chain credit, stablecoin/FX rails, ZK + interop infra, DePIN, and InfoFi/prediction markets, with clear specialization by fund.

Net takeaway

Across 2023–2025, crypto VC behavior matured significantly. The 2021-style FOMO cycle has ended; investors now prioritize fundamentals: revenue traction, unit economics, regulatory-ready architectures (KYC, custody), and cash-flow–aligned token design. The market is led by a small, disciplined core of crypto-native funds — Coinbase Ventures, YZi Labs, Gate Ventures, Big Brain Holdings, 1kx, Polychain, Pantera, Paradigm, Dragonfly, Multicoin, Framework — alongside a handful of returning institutional players in late-stage rounds.

Deployment has become high-conviction and selective: more capital into fewer but stronger teams, with clearer thematic alignment across CeDeFi, RWA, stablecoins/FX, DeFi infrastructure, and AI-adjacent systems. Early-stage syndicates continue to seed foundational protocols, while late-stage mega-deals are increasingly reserved for regulated exchanges, prediction markets, and institutional asset managers.

The chaotic “spray-and-pray” era is over. The funds that survived the 2022–2023 downturn now set the tone for the industry, and their synchronized theses with TradFi capital will heavily shape allocation patterns heading into 2026.

7. Structural Drivers & Narrative Outlook for 2025–2026

What drove the fundraising trends in 2025, and what narratives are investors betting on for the future?

A confluence of structural forces – regulatory developments, macroeconomic shifts, technological breakthroughs, and evolving user demand – underpinned the patterns we’ve discussed. These factors also inform the market narratives that VCs are coalescing around as we approach 2026. Below, we outline the key drivers and emerging narratives:

Macro & Regulation → Capital Rotation

The 2025 funding pattern reflected a clear alignment of regulation, macro conditions, and product readiness. As jurisdictions clarified rules (Singapore, HK, EU; later the U.S. via ETFs and policy shifts), capital rotated into compliance-heavy sectors—custody, CeDeFi, payments, RWA—and reopened the door for institutional-sized late-stage rounds.

With rates peaking and liquidity stabilizing, investors moved out the risk curve, producing fewer deals but larger tickets, concentrated in verticals where policy clarity + macro carry + institutional distribution intersected.

Infrastructure Maturity → Capital Moves Up the Stack

By 2025, Ethereum L2s, new L1s/appchains, modular stacks, and production-grade middleware removed the bottlenecks of earlier cycles. Infra deals split into:

- Scale-out infra (late-stage L1/L2, mining, compute, data)

- Frontier infra (ZK, On/Offchain, interop)

As infra became “good enough,” capital shifted upward into exchanges, asset managers, payments, RWA, and prediction markets—the layers that convert scalability into real users and revenue. These five sub-sectors absorbed ~50% of all capital raised 2023–25.

Product-Market Fit: Stablecoins, RWA & Info Markets Lead

By 2025, PMF was decisive.

• Stablecoins & payments: strongest global PMF; multi-billion late-stage rounds.

• RWA & structured yield: tokenized T-bills, credit, commodities moved from pilot → distribution.

• Prediction markets/InfoFi: treated as core market infrastructure, not speculation.

Meanwhile, low-PMF sectors (metaverse, forks, token-first social) saw capital vanish; gaming/NFT funding shifted to studios and infra. The funding bar heading into 2026: real users, real revenue, real retention.

Institutionalization & the CeDeFi Convergence

The 2025 capital stack became institutional. Large crypto-native funds, banks, sovereign wealth, and corporates wrote the biggest checks—mainly into regulated exchanges, asset managers, custody, payments, mining, and prediction markets.

They preferred equity-like structures, compliance rails, and RWA/CeDeFi products aligned with existing financial distribution. IPOs and M&A re-emerged, pushing late-stage capital toward CeDeFi, where licensed entities combine CeFi scale with on-chain settlement.

By 2026, late-stage activity will cluster around CeDeFi, RWA, stablecoins/payments, and regulated information markets, while early-stage funding continues seeding AI, ZK, DePIN, and next-gen infra.

Sectoral Narratives Shaping 2026

Gate Ventures’ vision: link

Outlook: A Higher-Quality, Narrative-Driven Growth Phase

Pulling these drivers together, the 2026 outlook is cautiously optimistic but clearly quality-biased. If 2023–24 was about survival and balance-sheet repair, and 2025 was about rebuilding confidence and recapitalizing the core rails, then 2026 is set up as a pragmatic growth year:

- Total funding can plausibly exceed 2025’s levels, but with continued concentration in fewer, larger, institutionally-owned deals.

- The marginal dollar is more likely to go into CeDeFi, RWA, Yield optimization, Payment/FX rails, regulated exchanges, prediction markets, compliance/identity infra than into speculative consumer apps or unsustainable tokenomics.

- Narratives around AI agents, BTC ecosystem expansion, DePIN, and decentralized social will drive early-stage experimentation, but capital will reward those that clearly connect to the core financial stack rather than purely to hype.

For funds and LPs, this environment rewards clear thematic maps and disciplined underwriting: understanding where each sub-category sits in the regulatory, macro, and infra stack; sizing exposure accordingly; and treating narratives as capital allocation frameworks, not just marketing. If regulation and macro stay broadly constructive, the bets placed in 2023–25 on the rails – stablecoins, CeDeFi, RWA, prediction markets, and compliant infra – are likely to form the spine of the next expansion phase in crypto venture.

Reference

The analysis above is supported by data and insights from Gate Ventures’ internal funding dataset (2023–2025 deals), augmented by industry reports, data providers and news

Crypto & Blockchain Venture Capital Q3 2025 | Galaxy

State of Crypto Fundraising: Q3 2025 – Messari

Prediction Market Kalshi Raises $1B at $11B Valuation in Mega …

State of Venture Capital in Crypto, Q1 2025 – CryptoRank

2024 Crypto Venture Capital Trends – insights4.vc

About Gate Ventures

Gate Ventures, the venture capital arm of Gate.com, is focused on investments in decentralized infrastructure, middleware, and applications that will reshape the world in the Web 3.0 age. Working with industry leaders across the globe, Gate Ventures helps promising teams and startups that possess the ideas and capabilities needed to redefine social and financial interactions. Website | Twitter | Medium | LinkedIn

Disclaimer:

The content herein does not constitute any offer, solicitation, or recommendation. You should always seek independent professional advice before making any investment decisions. Please note that Gate Ventures may restrict or prohibit the use of all or a portion of the services from restricted locations. For more information, please read its applicable user agreement.

The post Before the Breakout: How Capital Repriced Crypto for 2026 — From Winter to Infrastructure appeared first on BeInCrypto.